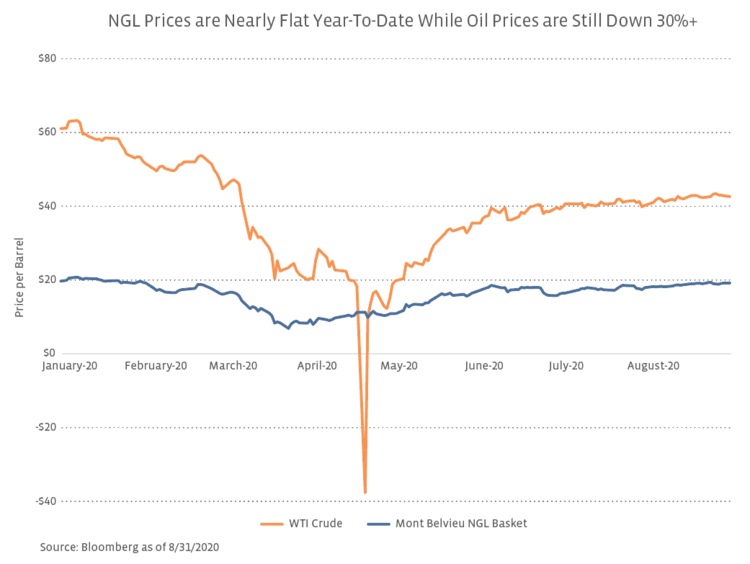

The swing in the Mont Belvieu, Texas, NGL basket price has been even more pronounced than that of natural gas, moving more in line with WTI crude. Since reaching a relative low of $6.91 per barrel (bbl) in late-March, NGL prices have increased by 177.8% and are now only down 2.6% on the year through the end of August. This resilience has been led by year-to-date price gains for ethane (39.9%) and propane (24.8%) prices, which together represent 70% of the typical NGL barrel. Since May, NGL barrel prices have remained within a range of ~40-60% of WTI prices, with the NGL basket price representing 45.5% of WTI prices at the end of August. For context, NGL prices were 32.3% of oil prices at the beginning of the year after averaging out at 37.2% of oil prices during 2019. This relative strength, much like with natural gas, has resulted from a tighter supply-demand balance. While the Energy Information Administration (EIA) expects overall consumption of hydrocarbon gas liquids, which includes NGLs and olefins, to fall by 1.3% in the US this year, declines are much more muted than those of other petroleum products like motor gasoline, diesel, and jet fuel. Additionally, US consumption is expected to increase by 6.5% in 2021 on a year-over-year basis. Looking globally, Enterprise Products Partners (EPD) noted on its most recent earnings call that even at the peak of the pandemic, demand for liquefied petroleum gas (LPG) exports, which includes the NGLs ethane and propane, were near record highs for its facilities. Management credits this strength in demand to a desire for quality-of-life improvements in other areas of the world that come from NGLs, including plastics and heating.

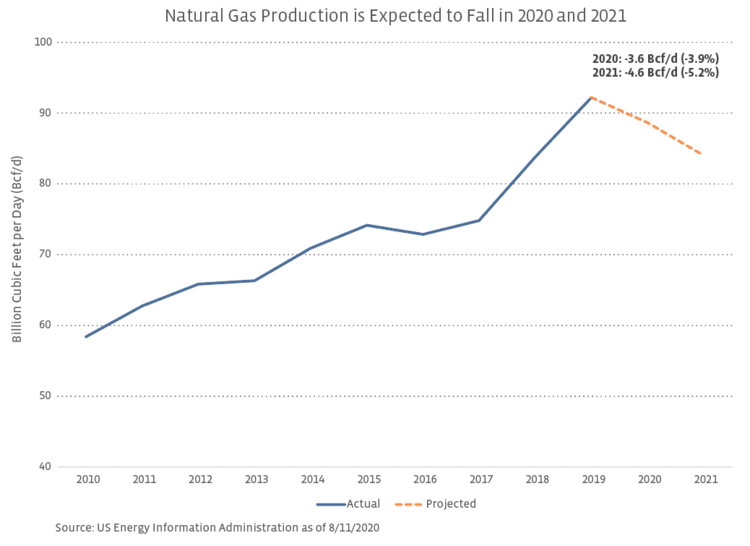

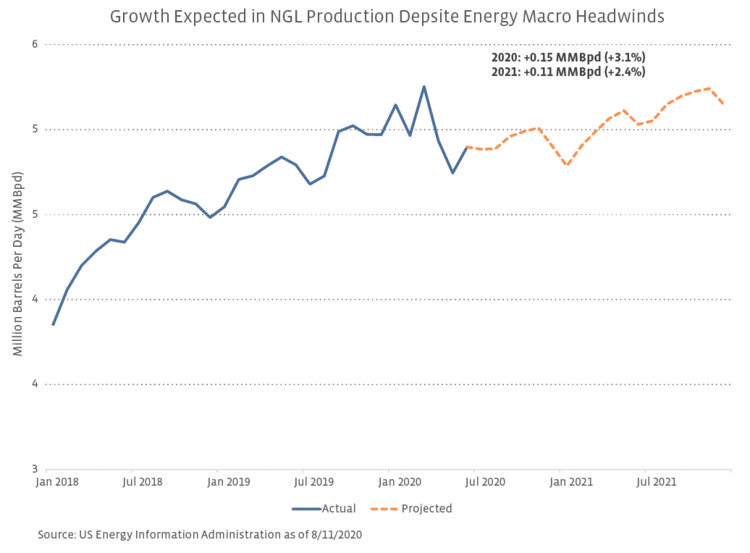

Forecasts point to natural gas production decline, but NGL production expectations are constructive.

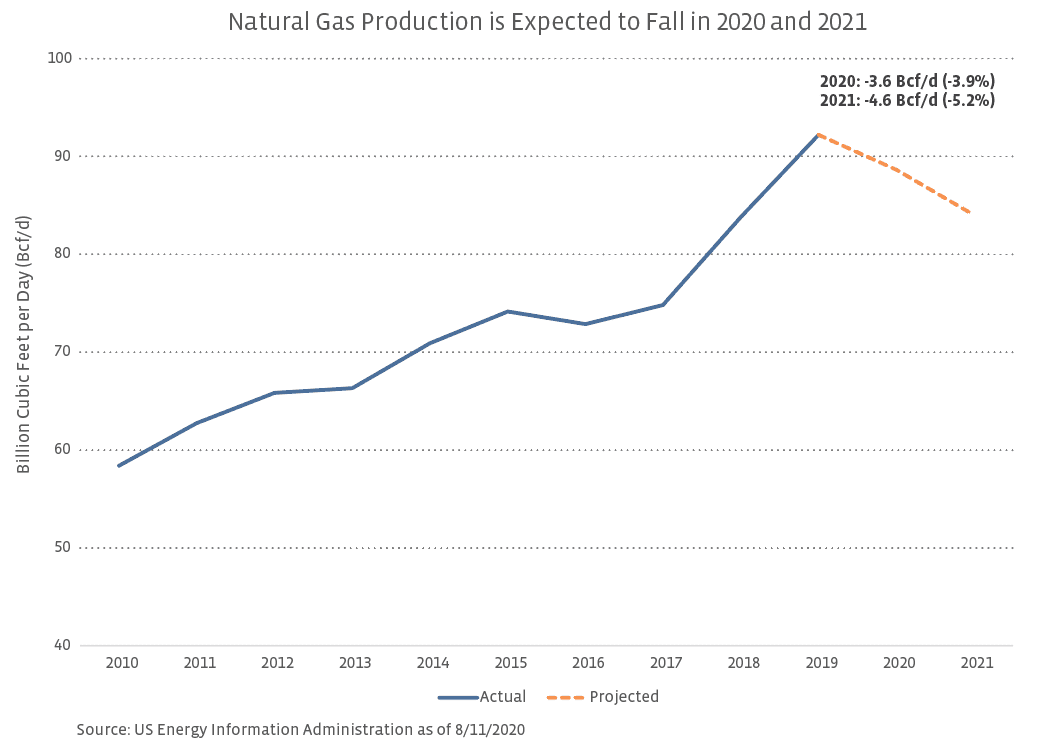

Despite the improvement in prices, natural gas production forecasts remain somewhat underwhelming. Per the EIA’s most recent Short-Term Energy Outlook, dry natural gas production is expected to decline by 3.9% this year and 5.2% in 2021. Average forecasted 2021 production of 84.0 billion cubic feet per day (Bcf/d) is roughly in-line with 2018 levels. Note that these forecasts were published on August 11 and do not entirely account for last month’s price increase, and the next Short-Term Energy Outlook, set to be released tomorrow, may show improvement. Additionally, natural gas production was already expected to moderate coming into 2020 as historically weak prices caused producers to pull back on growth (read more). In a reversal of expectations prior to COVID-19, oil production is expected to see slightly worse declines than natural gas over the next two years, with 2021 production estimated to be 9.0% below 2019 levels.

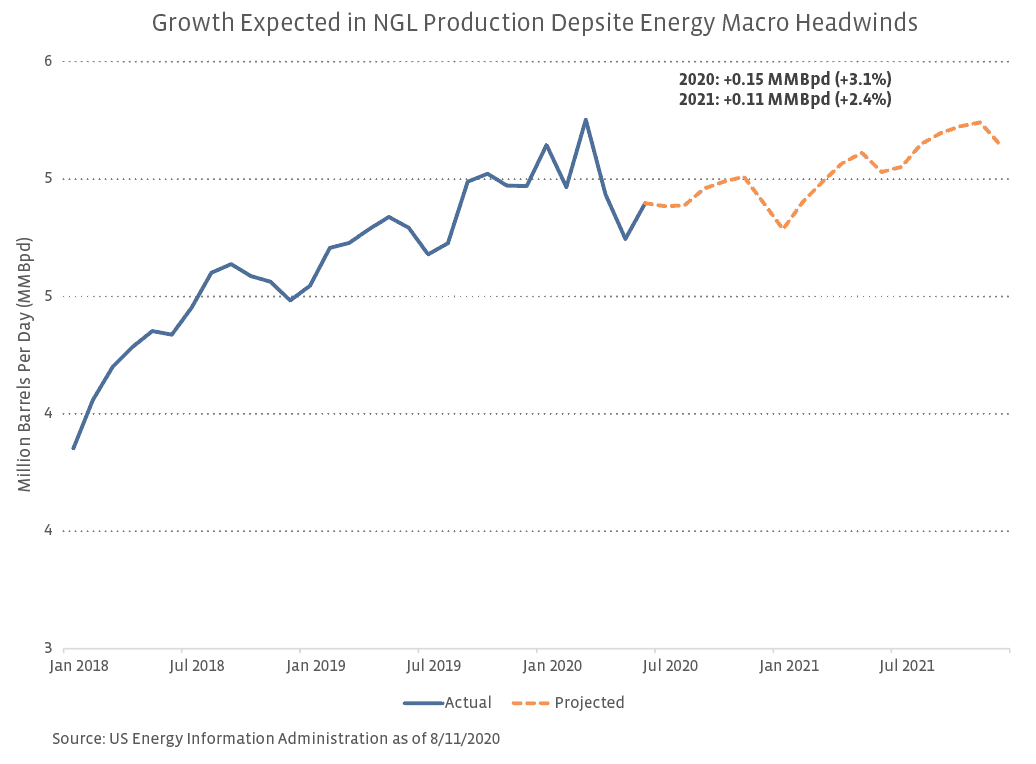

NGL production expectations paint a much different picture. The EIA is projecting 5.4% growth in natural gas liquids production from 2019 through 2021. These forecasts have seen notable positive revisions in recent months amid the backdrop of improving fundamentals. The EIA was forecasting slight year-over-year production declines in both 2020 and 2021 as of early June (read more). In the short-term, volumes will likely continue to recover as wells are brought back online. Resilient demand for NGLs will help drive production, with ethane recovery playing a key role in increasing NGL production in the face of lower oil and natural gas volumes. Field production of ethane reached a record high of 2.1 million barrels per day (MMBpd) in June, and the EIA expects full-year ethane production to average 2.2 MMBpd in 2021, representing a 20.2% increase from 2019 levels. EPD’s management noted increased ethane recovery in the Rockies during 2Q, helping to reinforce these new highs. On its 2Q20 earnings call, ONEOK (OKE) highlighted a return to pre-COVID NGL volumes at its facilities partially led by higher ethane recovery in the Mid-Continent. This strength is expected to continue throughout 2020 as ethane economics remain favorable. DCP Midstream (DCP) also reported flat NGL volumes on a sequential basis in 2Q20 as a result of increased ethane recovery. The partnership noted that continued ethane recovery could represent a potential tailwind for the business in the back half of this year.

What are the implications for midstream?

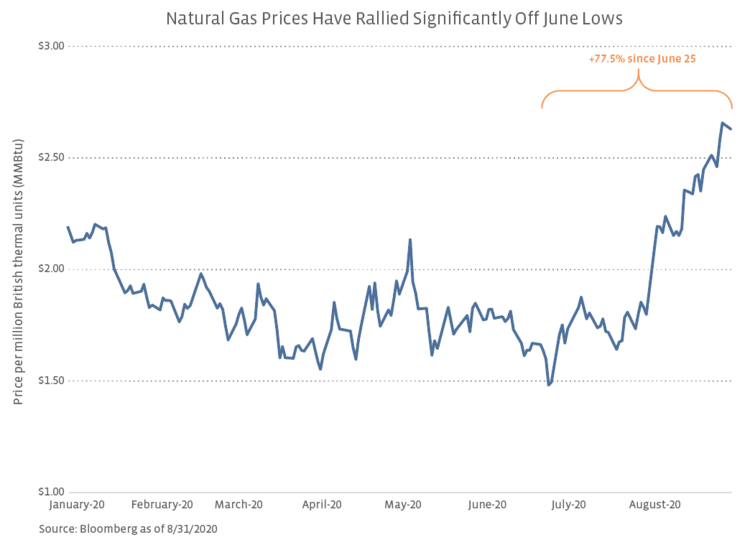

Energy infrastructure companies stand to benefit from improving natural gas and NGL fundamentals in a few key ways. First, the rally in natural gas prices has driven equity price improvement for gas-levered midstream names. While the fee-based nature of midstream cash flows helps mitigate the impact of price fluctuations for oil or gas, higher natural gas prices can help drive positive sentiment. For the month of August, gathering and processing was the best performing subsector of the Alerian Midstream Energy Index (AMNA), and the five best-performing constituents were all gathering and processing names. Year-to-date, liquefaction and natural gas transportation have been the standout performers in AMNA, with natural gas transportation names outperforming petroleum transportation names by ~470 basis points on an equal-weighted basis through August 31. As associated gas volumes lag due to lower crude production, companies with assets serving dry gas plays may enjoy a tailwind relative to their oil-weighted peers. On its 1Q20 earnings call, Kinder Morgan (KMI) noted that it could see incremental activity in its Haynesville system later this year or in early 2021, potentially offsetting weakness in other areas. Natural gas infrastructure will also play a critical role in facilitating the growth of US gas exports and will benefit from the constructive long-term outlook for liquefied natural gas demand (read more).

NGLs in particular are a current bright spot for midstream companies. As discussed above and in our 2Q20 Earnings Review (read more), many companies highlighted the health of NGL volumes in recent earnings reports. Going forward, projected production and global demand growth may create opportunities for the build out of additional NGL infrastructure. Several projects are currently in the works or recently came online. Last week, Energy Transfer (ET) announced completion of an expansion of its Lone Star Express Pipeline ahead of schedule. The new 352-mile pipeline connects to the larger Lone Star Express Pipeline and will add over 400-thousand barrels per day (MBpd) to ET’s existing Texas NGL pipeline network. Having completed several NGL projects so far this year, including an expansion of its Galena Park LPG export facility, Targa Resources (TRGP) expects its 110-MBpd fractionation Train 8 at Mont Belvieu to enter service this quarter and its Grand Prix NGL Pipeline to enter service in early 2021. Separately, MPLX (MPLX) has formed a joint venture with WhiteWater Midstream and West Texas Gas to provide NGL takeaway capacity from southeast Texas that leverages a mixture of existing infrastructure with some new construction for capital efficiency. To be clear, NGL projects have not been immune from the project cancellations and deferrals that have taken place so far this year as companies preserve financial flexibility and recalibrate plans for the current production outlook. For example, MPLX decided not to pursue its Belvieu Alternative NGL Pipeline (BANGL), which would have provided NGL transportation from the Permian Basin to the Texas Gulf Coast, and deferred the fractionation and export capacity associated with it. Continuation of a supportive macro backdrop could result in additional growth opportunities for midstream, whether related to transportation, fractionation, or exports.

Bottom Line

Midstream exposure to natural gas and natural gas liquids is often underappreciated as oil fundamentals garner greater attention, but as of August 28, the broad AMNA Index was 67.9% weighted to companies primarily focused on natural gas gathering, processing, transportation, or liquefaction. The rebound in natural gas prices and resilience of NGL fundamentals mark relative bright spots in the current energy landscape with positive implications for supporting midstream infrastructure from pipelines to export facilities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}