Not All MLPs Have Toll-Road Business Models

In the same way that every MLP business isn’t the same, not all gas processing contracts are the same. Some are more sensitive to commodity prices than others. While there has been a greater shift to fee-based processing contracts over the past several years, there are actually three other types of processing contracts you need to know about: keep-whole, percentage of proceeds (POP), and percentage of liquids (POL). Some MLPs might have a diverse group of contracts due to economics differing by region. As an MLP investor, understanding the different risk profiles is beneficial in decision making.

Keep-Whole Contracts

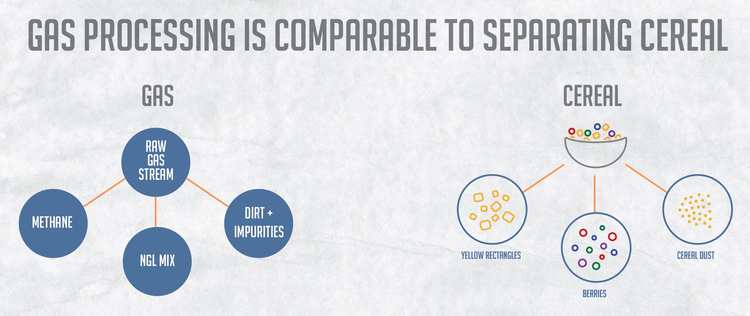

To explain keep-whole contracts, let’s go back to the Captain Crunch with Berries. Imagine that my husband, Jon, learns there is a market for separated cereal and decides to start up a side-hustle. I buy him a box of cereal at the store so he can start his “business”. Let’s say all the cereal in the box contains 1,000 calories and costs $2.00. Jon removes 400 calories worth of cereal (all the berries), keeps them for himself, and returns the remaining 600 calories of rectangular pieces to me. I give him the option to either (1) give me $0.80 to pay for the berries he removed, or (2) find a way to return 400 calories to the box in yellow rectangles, so that I am “made whole” on my original purchase. Jon settles with me, and then sells the group of berries for more than $0.80 on Craigslist.

Now, while it’s a bit bizarre, the cereal side-hustle is very similar to what happens with natural gas processing keep-whole contracts. In the example above, think of me as the producer and Jon as the MLP. Producers give their raw natural gas to the MLP to be processed. In the same way that Jon extracted the berries from the cereal, MLPs extract NGLs and then sell them (hopefully) at a profit. Jon kept me whole by giving me back the rectangles he wasn’t selling and giving me $0.80 for the calories he took. MLPs keep producers “whole” by either returning an equivalent BTU content (think of this as the “caloric value of heat content”) in methane to match what they were originally given or by paying for the units of energy they extracted or retained.

Keep-whole contracts are the most commodity sensitive. Since NGL prices have historically been closely linked to the price of oil, keep-whole contracts make lots of sense when the crude-to-gas ratio is higher. Because of pricing and buyer risk, MLPs with keep-whole exposure generally try to lock in prices for their expected NGL volumes via hedges, thereby reducing the risk of not having a buyer, or a buyer who changes the price at the last minute. Anyone who has sold anything on Craigslist knows the frustration of either scenario.

That said, NGL hedges tend to be traded less often than natural gas prices, so it can be difficult to secure hedges on NGLs for more than one to two years out, or even secure hedges for large quantities of NGLs. Because current oil prices are markedly lower than they were two to three years ago, the cash flow for MLPs with keep-whole contracts have been the most impacted.

POP and POL Contacts

With POL contracts, the MLP is paid in the form of a percentage of the liquids recovered, and the producer bears all the cost of the natural gas shrink. This would be akin to me buying the Captain Crunch, giving it to Jon to separate, and letting him keep some of the berries as payment for his separating work.

With POP agreements, the MLP receives a percentage of the proceeds from the sale of natural gas and NGLs. As a result, the MLP is long both the price of NGLs and natural gas. To relate it back to our cereal story – I buy the box, Jon separates it, I sell the components, and give him a portion of the money I make.

POP and POL contracts are not as commodity sensitive as keep-whole contracts, but not quite as agnostic as fee-based contracts.

Fee-Based Contracts

Along with being the least sensitive to commodity prices, fee-based contracts are also the most straight forward. MLPs process the natural gas for a producer and charge them a set fee for the work. In other words, Jon separates the cereal for me, I pay him for his labor, and I sell the pieces.

Contract Types Shift Over the Years

Currently, the contract structure that management teams brag about in presentations are fee-based contracts. In the current commodity environment, investors may prefer it because regardless of the price of the commodity, the MLP makes money. However, should oil suddenly start rising back into triple digits, don’t be surprised if keep-whole and POL contracts come back into favor. Investors may disregard the stability they currently prefer in favor of upside earning potential from higher NGL prices.

Questions about energy are important, y’all. Just ask Ken Bone who is now famous for asking an energy-related question during the October 9th Presidential Debate and looking adorable while doing so. Keep your questions coming by emailing [email protected]! Next week, we’ll talk about what happens when Jon takes the berries and separates them out further into red, blue, purple, and green berries, known as fractionation.