AMZ and AMZI Q/Q Fun Facts

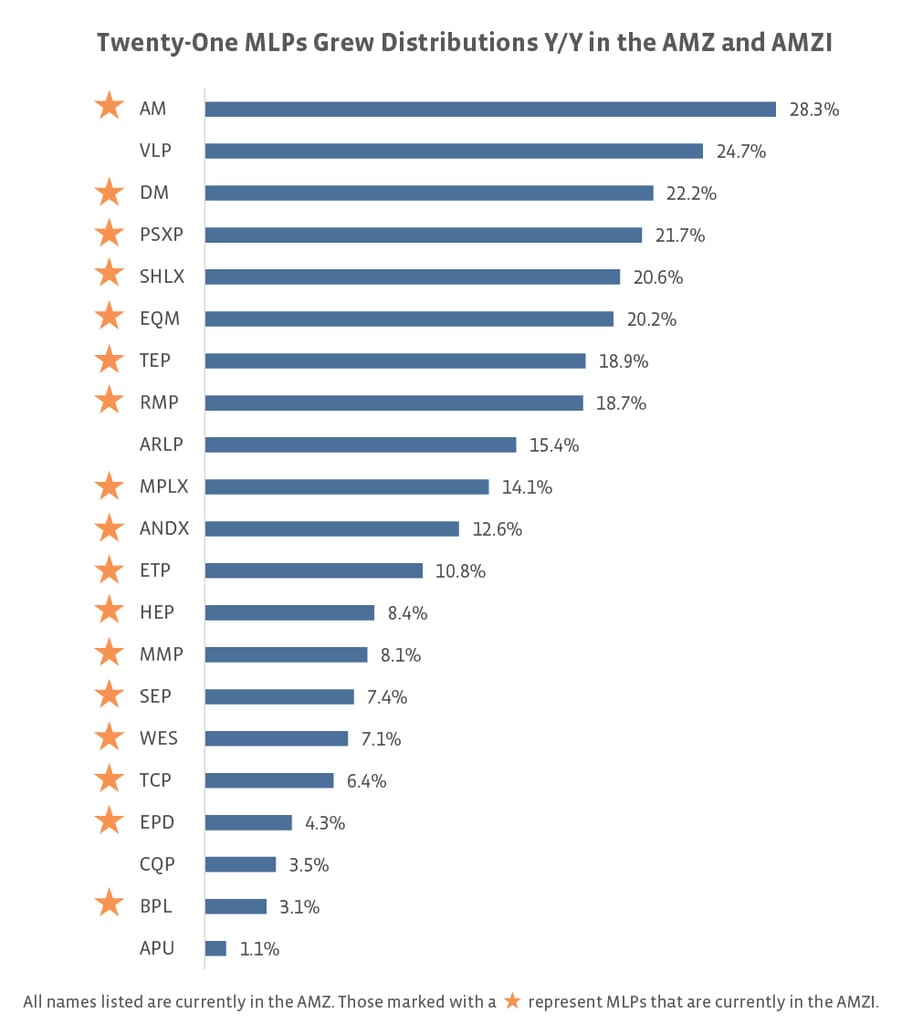

Antero Midstream Partners (AM) won the percentage increase contest this quarter with a 6.25% bump from $0.32 to $0.34.- Including AM, there were four companies that increased distributions by 5% or more: Valero Energy Partners (VLP), Phillips 66 Partners (PSXP), and Dominion Energy Midstream Partners (DM).

- Of the 15 MLPs that grew distributions in the AMZI, six increased payouts by 4% or more: AM, PSXP, DM, EQT Midstream Partners (EQM), Shell Midstream Partners (SHLX), and MPLX (MPLX).

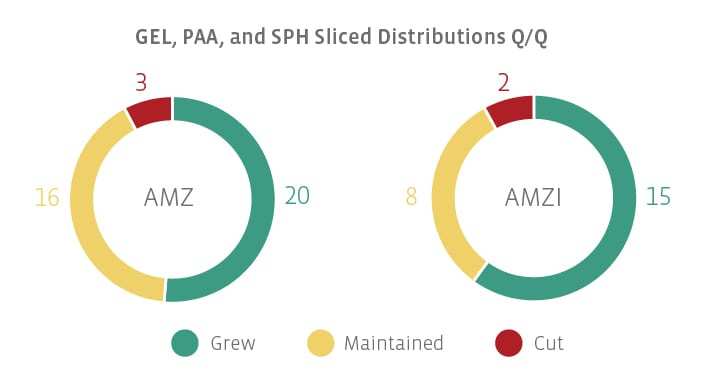

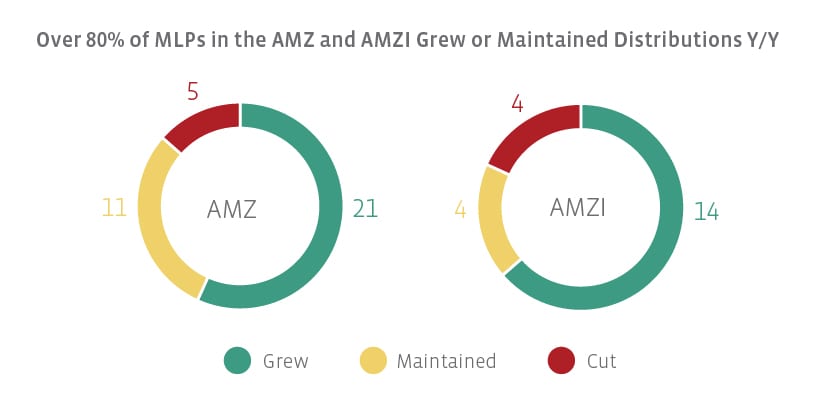

Next, we have the year over year data, which compares 3Q 2016 and 3Q 2017. If the name was in the index in both 3Q 2016 and 3Q 2017, I compared the distributions. DM, Holly Energy Partners (HEP), and Rice Midstream Partners (RMP) are excluded from the AMZI pie chart shown below because they were not constituents of the index in 3Q 2016 (although they are current constituents). Please note there is survivorship bias in this method.

- Names that maintained year over year (all names listed are in the AMZ, those with a * represent MLPs that are also in the AMZI):

Boardwalk Pipeline Partners (BWP)

Crestwood Equity Partners (CEQP)

DCP Midstream Partners (DCP)

Enable Midstream Partners (ENBL)

EnLink Midstream Partners (ENLK)

Golar LNG Partners (GMLP)

NGL Energy Partners (NGL)

NuStar Energy (NS)

Summit Midstream Partners (SMLP)

Sunoco (SUN)

Teekay LNG Partners (TGP)

Those that cut year over year were Plains All American Pipeline (PAA), Enbridge Energy Partners (EEP), Suburban Propane Partners (SPH), Williams Partners (WPZ), and Genesis Energy (GEL).

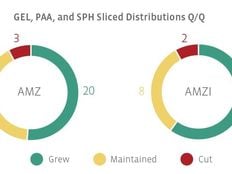

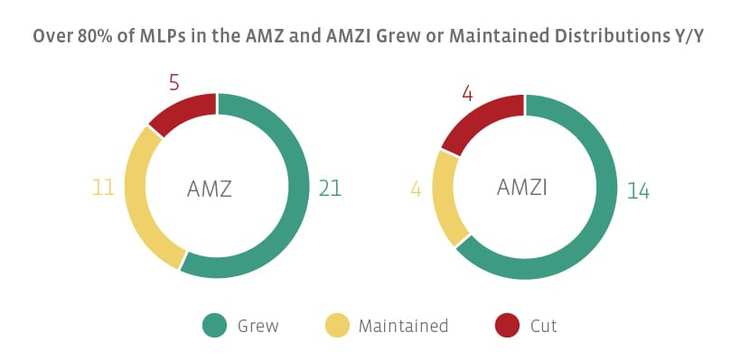

As mentioned, GEL, PAA, and SPH each cut their distributions for 3Q 2017. PAA had telegraphed their distribution cut back in August, indicating that the distribution would be reset to align with PAA’s fee-based segments, and cash flows from the Supply & Logistics segment would not be included in the calculation. PAA’s cut is noteworthy because the distribution had already been cut for the third quarter of 2016. This has reasonably raised eyebrows among stakeholders and caused concern for many investors. SPH and GEL discussed strengthening the balance sheet and enhancing financial flexibility in the context of their cuts. For additional commentary and analysis of GEL and SPH’s cuts, check out my colleague’s “What Happened in October” post.

While distribution cuts tend to generate more headlines, it’s important to keep in mind that many MLPs continue to grow their distributions, including some increasing their distribution by 4+% on a quarter-over-quarter basis. That kind of growth is nothing to sneeze at!

{kind=link}

{kind=link}

{kind=link}