Everyone who can get to the track can bet on horse races. If you learn about horses and racing, stay informed, bet on the right horses, and get a little lucky, you can make money. But if you own the thoroughbred, or even part of one, you can make significantly more money (you’ll also take on greater risk). Purse money can be $25,000, but it can also be in the millions.

Horse racing is an enormous gamble, which is why our analogy can only take us so far. Horses are delicate, even fragile. One injury, a single misstep, can derail their entire careers. Midstream MLPs, on the other hand, are involved in the much more robust business of building and operating energy infrastructure. A shipment of steel delivered one day late, a welder fallen ill and unable to work, even a pipeline leak will not implode the entire business.

Owning units of an MLP GP is a bit like owning part of the horse (minus, of course, the continual cost of training and shoeing). You don’t get to help make decisions, but when the underlying LP wins acquisitions and builds assets that grow the distribution, you have leveraged participation in that growth. But you also participate in forgoing growth and have greater downside risk, should the MLP run into trouble.

If this analogy is totally lost on you, maybe it’s because I’ve only ever bet on a handful of horse races in my life. Please visit the MLP University if you don’t know what a GP of an MLP is, why it might be lucrative, or why it might weigh down an MLP. Got the basics? Awesome. We’re going to start with some history.

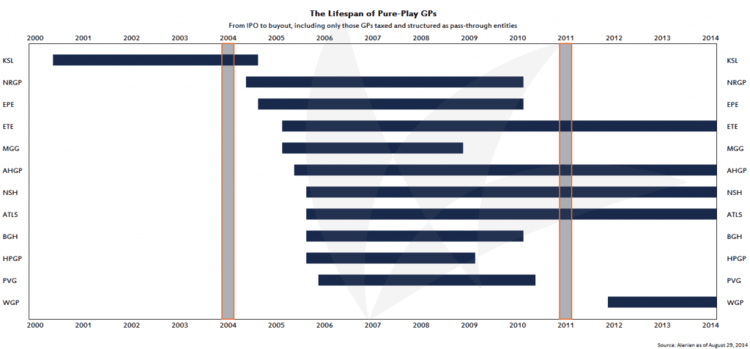

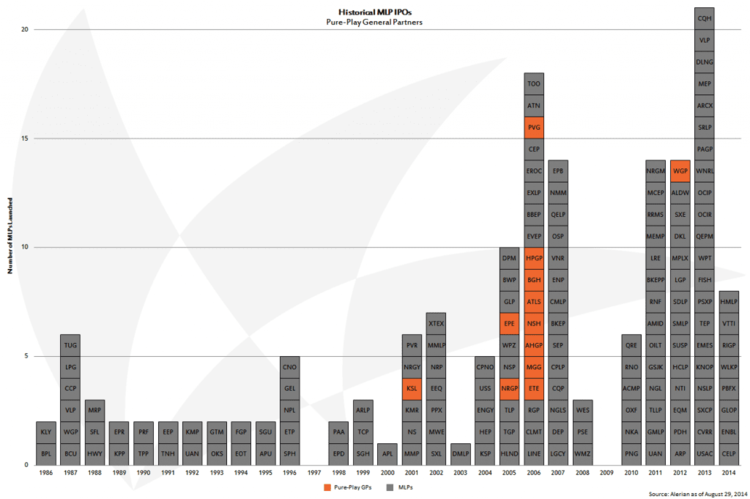

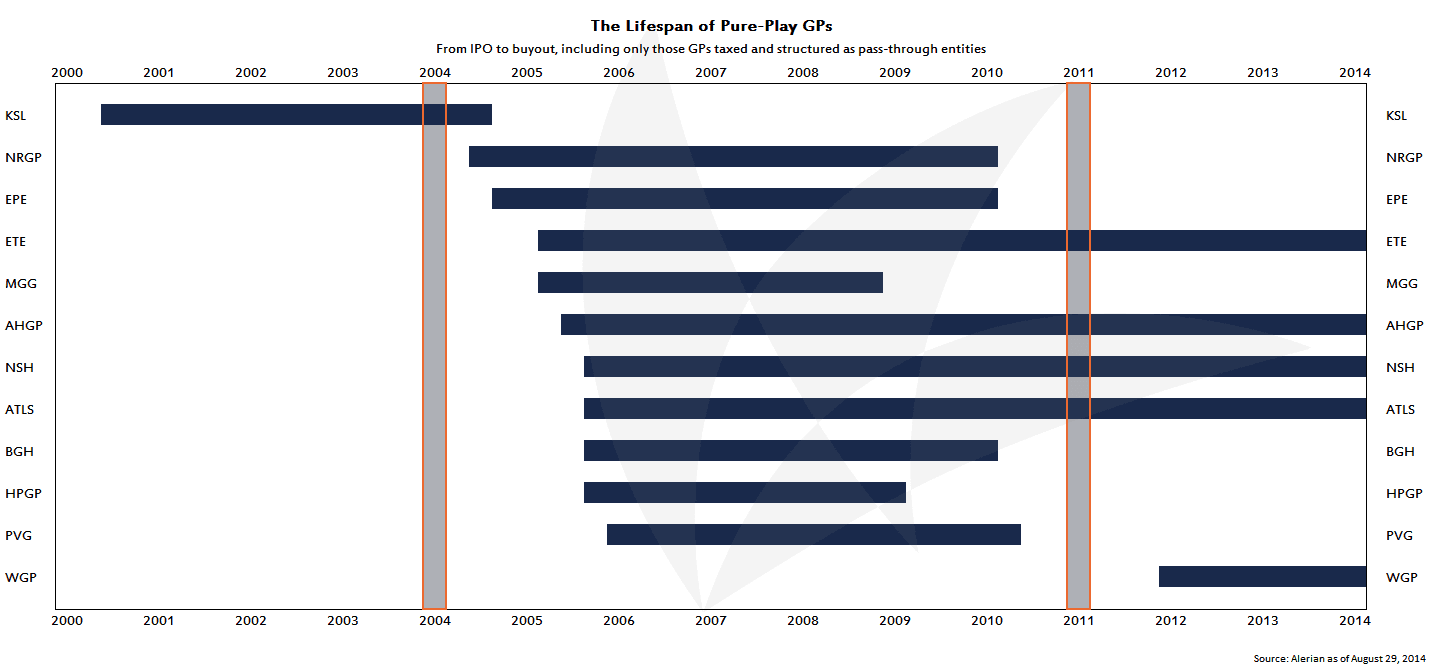

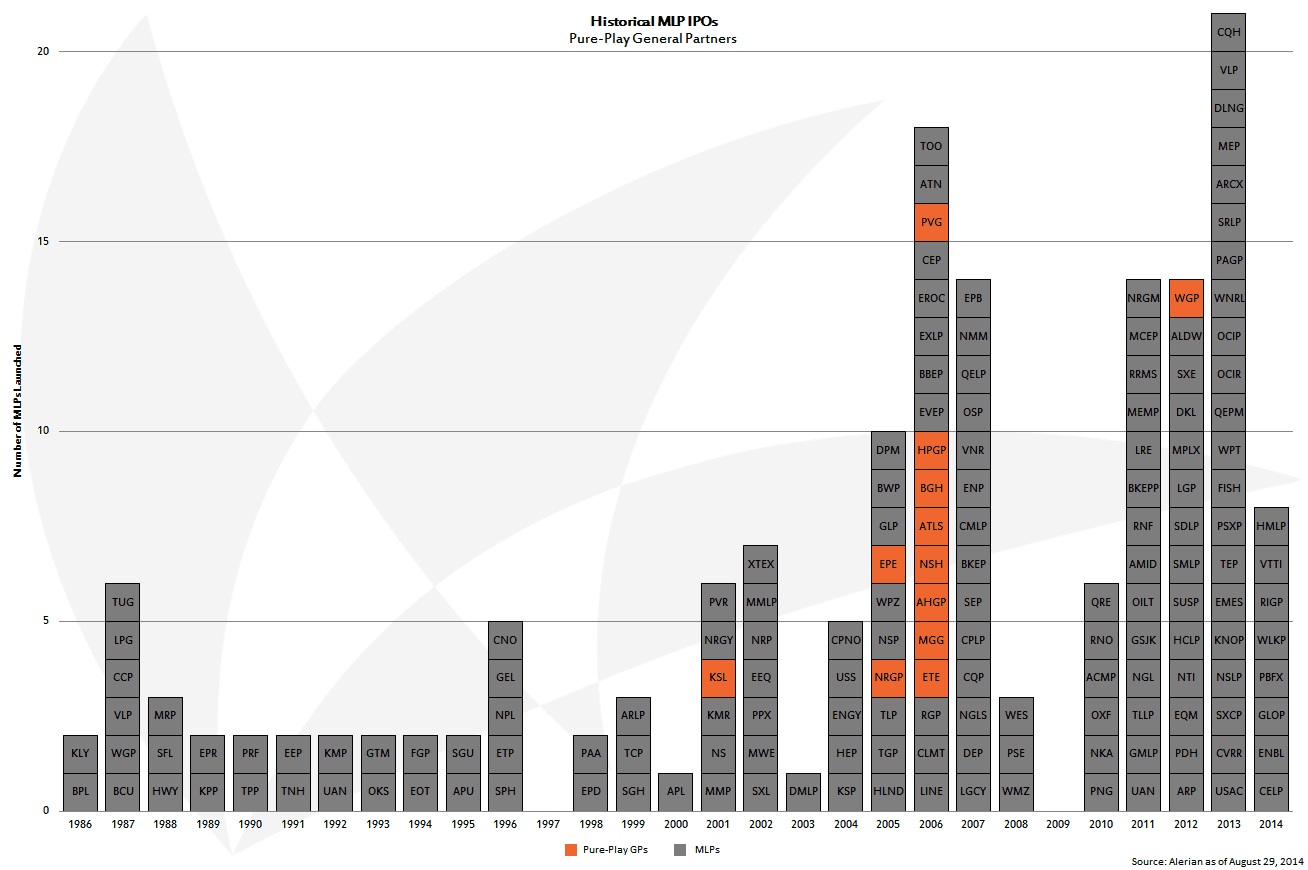

MLPs may have been around since the 1980s, but pure-play GPs were not investable by the general public until June 29, 2001, when Kaneb Services (former ticker: KSL) completed its IPO. Many GP IPOs came a few years later, in 2005 and 2006.

What made that time period so special? Well, with the turn of the millennium, MLPs just started to gain enough ground to be identified as a separate, emerging asset class. At the start of 2000, there were just 24 MLPs with $11 billion in market capitalization. Three years later, there were 34 MLPs with $28 billion in market cap. MLPs then proceeded to return 45% and 17% in 2003 and 2004, respectively, on a total return basis, sparking additional interest in them. Since GPs have leveraged exposure to LP distribution growth, and LPs were growing their distributions by more than 6% on average, some investors (or at least the bankers) began to recognize the value in owning a piece of the GP, provided there was conviction about the underlying LP’s business prospects. GPs that went public were typically at or near the 50/50 splits, making the benefit of leverage that much more visible in the near term.

Of the 10 GPs that completed their IPOs in 2005-2006, six were acquired by their LP in 2009-2010. That’s too much of a pattern to ignore. What changed? For starters, there was the financial crisis and attendant headwinds. With restricted access to the capital markets, growth became a much more difficult proposition. Add to that the burden of a GP’s disproportionate take on acquisitions and organic projects, and some companies saw their distribution growth grind to a halt. An MLP without a GP can afford to earn a slightly lower return on its investments, which enables it to bid a little more. Additional benefits to purchasing one’s GP include simplifying the organizational structure, increasing liquidity (as it is now one larger company, instead of two smaller ones), and avoiding any potential risk of a change to carried interest taxation (which, depending on the proposed language, could affect IDRs held by GPs structured as pass-through entities).

Obviously, each story, like each horse, is different. Next week, we’ll compare the performance of companies that acquired their GP and companies that didn’t.

{kind=link}

{kind=link}