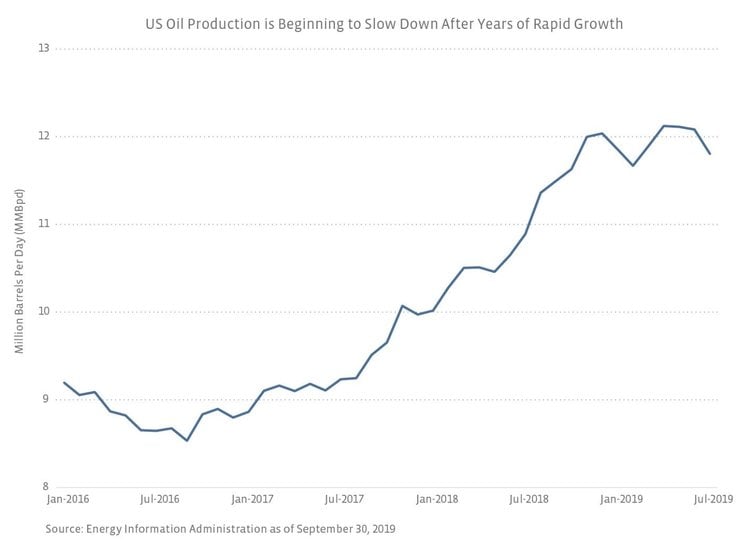

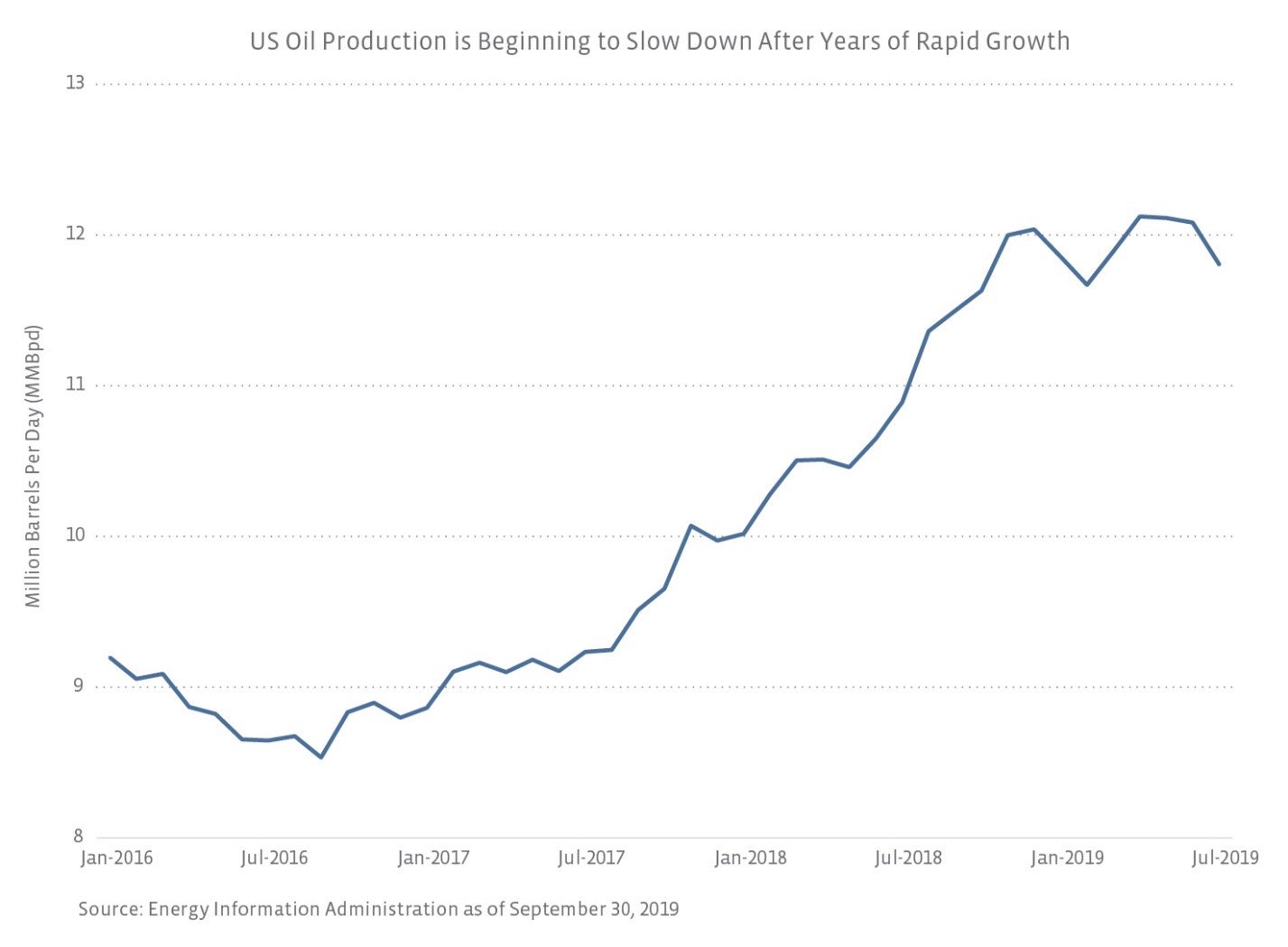

While oil prices remain above the levels seen in late 2015 through 2016, lower WTI prices have contributed to the recent production slowdown. Independent exploration and production companies (E&Ps) are practicing more capital discipline in order to drive returns in a relatively modest price environment, with WTI in the $50s per barrel (bbl) range. On its 2Q19 earnings call, Permian pure-play producer Diamondback Energy’s (FANG) management team noted that the company, although still increasing production in 2020, would no longer be maximizing growth in order to drive cash flow generation. Concho Resources (CXO) initially guided to 2019 capital spending of $3.5 billion at the midpoint but pulled back their budget to $2.9 billion to drive cash flows in a lower crude price environment. As a result, CXO’s full-year 2019 production guidance was lowered from 29% to 24% at the midpoint. E&Ps reining in spending and consequently slowing down production growth are reflective of investor demands for better returns and free cash flow generation. Other factors that have weighed on production growth have been operational inefficiencies, such as the impacts of parent-child well interference in the Permian. These are wells that are drilled very closely to one another, resulting in a cannibalization of production (think two straws drinking from the same milkshake).

Large integrated producers, such as Chevron (CVX) and Exxon Mobil (XOM), have continued to expand production at healthy rates, investing heavily in US shale production. These companies are generally less sensitive to crude prices due to their large, diversified businesses and reliance on shale to propel overall production growth. XOM highlighted a significant investment in the Permian Basin at its 2019 Investor Day with the goal of reaching 1 million barrels of oil equivalent per day (MMBoe/d) of production from the basin by 2024. CVX management is guiding to 900 thousand barrels of oil equivalent per day (MBoe/d) of Permian production by 2023, which is more than double 2Q19 Permian production of 421 MBoe/d.

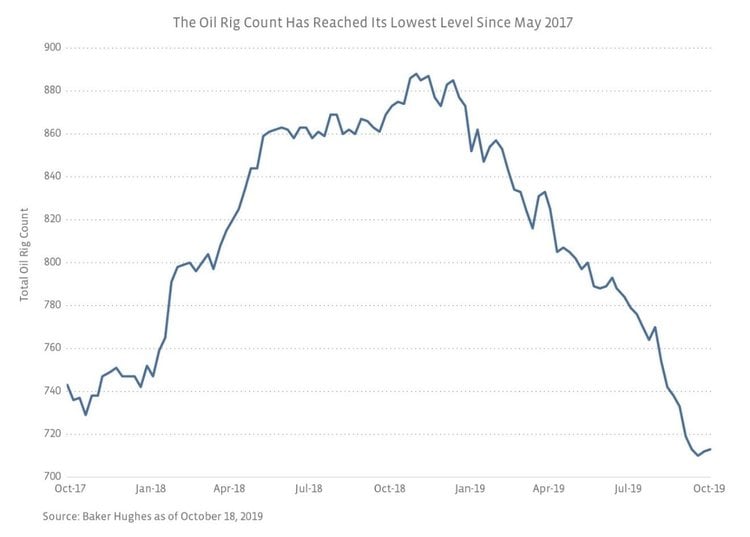

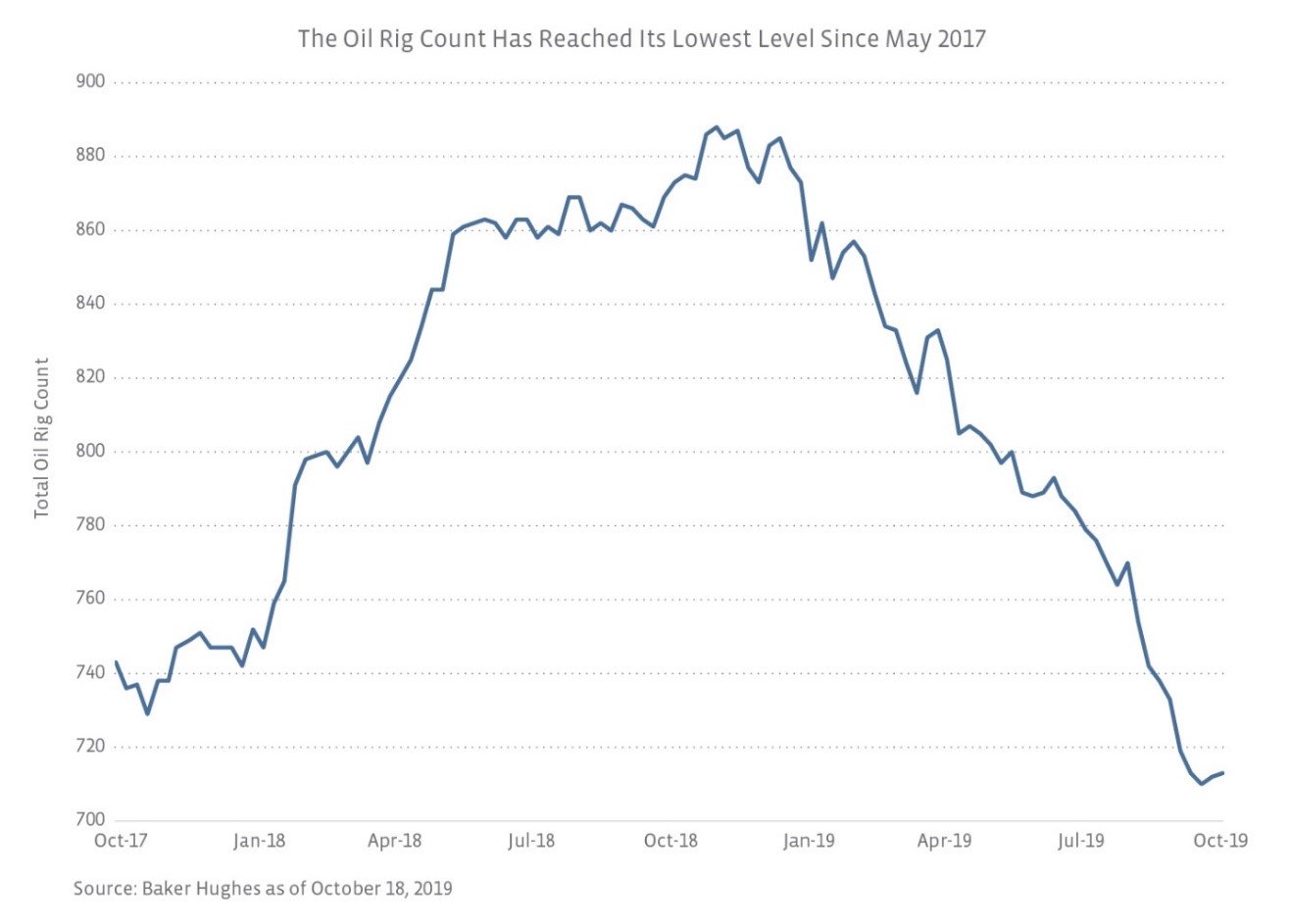

Market observers often look to the oil rig count for an indication of potential growth trends. The Baker Hughes North America rig count reached its lowest level since May 2017 earlier this month. As of October 18, there were 713 total active oil rigs in the US. This number represents a 19.4% decline from the beginning of the year and is, for context, 5.7% below the three-year average. Despite the decline in rigs, it is important to note that productivity improvements and increased efficiency mean that production growth can continue with fewer rigs (read more). Additionally, there are still 5,787 drilled but uncompleted (DUCs) wells in the more oily Permian, Bakken, and Eagle Ford basins. By basin, this breaks down as 3,668 DUCs in the Permian, 675 in the Bakken, and 1,444 in the Eagle Ford.

Looking ahead

Although the outlook may not be as robust as it has been in the last few years, oil production growth is still expected in the coming years; several industry players are still guiding to production growth through the remainder of the year and into 2020. In the EIA’s most recent Short-Term Energy Outlook (STEO), the administration forecasts that oil production will ramp up this quarter as a result of additional Permian takeaway capacity to the Gulf Coast and the resolution of disruptions in offshore drilling in the Gulf of Mexico. For full-year 2019, the EIA is guiding to an 11.8% (1.3 MMBpd) year-over-year production increase. Average production in 2020 is expected to be 13.2 MMBpd, representing a 7.3% (0.9 MMBpd) year-over-year increase. As the production base continues to climb, it becomes more difficult to grow annual production by double-digits percentages, but 1.3 MMBpd of growth in 2019 compared to 0.9 MMBpd in 2020 still represents a slowdown. Additionally, the EIA is forecasting average WTI crude prices of $56.26 per barrel (bbl) and $54.43/bbl in 2019 and 2020, respectively. Although the EIA partly attributes deceleration of growth in 2020 to lower crude prices, in addition to slower growth in well-level productivity, next year’s price forecast is not a meaningful departure from the current crude price environment. However, a material, sustained increase in crude prices could help drive more activity and subsequent production growth.

Beyond 2020, the long-term production thesis remains intact. In its Oil 2019 report, the International Energy Agency (IEA) forecasts that the US will continue to be a world leader in oil supply growth over the next several years. Through 2024, the IEA estimates that the US, driven by shale production, will account for 70% of global oil production growth and pass Russia in total exports in 2023. The Permian Basin will also continue to play a key role in rising oil production. During its 2019 Investor Day, Plains All American (PAA) estimated that Permian production will increase by over 3.3 MMBpd through 2023, accounting for over 65% of total North American oil production growth over that time period. While it does appear that the most rapid phase of growth may be coming to an end, the prospects for US shale production are still constructive.

How does slower production growth impact midstream?

Midstream companies have quickly built out energy infrastructure across the US over the last decade in order to meet demand from ballooning oil production. This build-out has required substantial capital spending. As production growth moderates, so will midstream capital expenditure expectations (read more). With lower capex budgets, midstream companies will be able to generate greater free cash flow and enjoy improved financial flexibility. Midstream companies could use those cash flows to strengthen their balance sheets, fund the equity portion of growth capital, sustainably increase distributions, or even buy back shares. To be clear, the expectation is that growth capital will moderate – not fall to zero. While the pace of production growth is slowing, US shale production continues to rise. Additional energy infrastructure will still be required to connect upstream production with demand, creating further opportunities for midstream companies and maintaining the long-term investment thesis for the space. Additionally, it is important to note that midstream companies have growth opportunities well beyond pipelines, including export facilities, gas processing plants, and even petrochemicals (read more).

Bottom Line

While US crude production growth may finally be showing signs of a slowdown, US shale production is still expected to grow in the high single digits next year. More broadly, the long-term thesis for US energy production and exports remains intact. Midstream companies, along with their upstream counterparts, can benefit from free cash flow harvesting that accompanies lower capital budgets and the cash flows generated by new infrastructure that has recently been placed into service.

{kind=link}

{kind=link}