For quite some time, MLPs and their cash flows have been touted as a way to protect against inflation. And, yes, while they get the benefit of rate increases when inflation goes up, it also goes the other way when there is deflation. Unfortunately, we can’t always have our cake and eat it too.

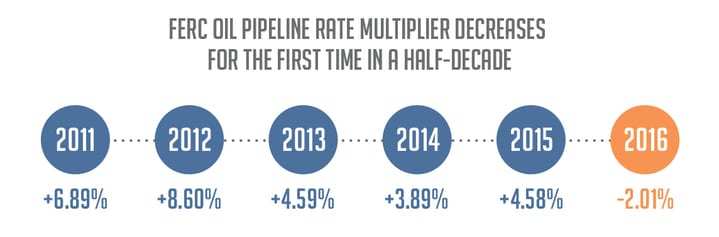

Now, if you had the energy to click back to my December mailbag, you were reminded that the current methodology will remain in effect until 2021. You also read my guess that lower pipeline costs and modifications the FERC made to its assumptions likely triggered the decrease from 2.65% to 1.23%.

Given how the commodity environment can change, you might be left wondering if there is any wiggle room for these rates. And, interestingly, while indexing as I am describing is the most common way of setting rates, there are three options for higher rates: cost-of-service, settlement rate, and market based rates. FERC approval of rates is required in all cases and isn’t necessarily guaranteed. Enterprise Products Partners (EPD) and Enbridge Inc (ENB), for example, sought approval to charge market based tariffs on their Seaway Crude Oil Pipeline in 2011. After lots of back and forth, the court eventually decided against the rate increase, citing failure to comply with the FERC’s “just and reasonable standard.” It’s important to remember, however, that there are options available should we see a dramatic market change in the next five years.