Leveraged ETFs are exchange-traded funds that use debt and derivatives to amplify the daily gains of an underlying index. These vehicles are still subject to market pressures of buying and selling, and while they are designed to mimic the daily returns of the underlying asset, they don’t match the underlying asset exactly. Below we look at some of the commonly asserted dangers of investing in leveraged ETFs.

Highly Volatile Environments Erode Value

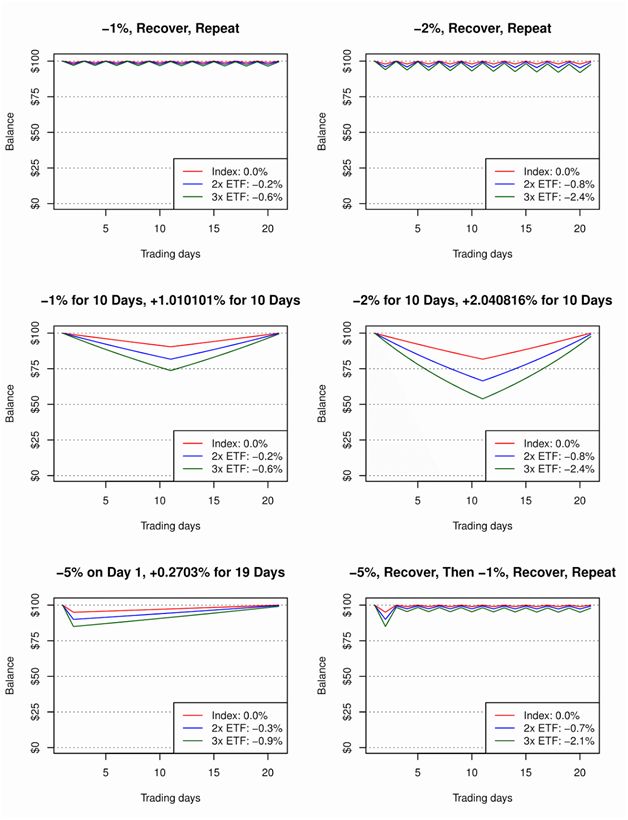

It has almost become common street knowledge that holding a leveraged ETF in a market with high volatility and a horizontal direction can destroy the share value. The erosion in asset value has become so well known that it has spawned many names: “leveraged decay” and “volatility drag” to name a few — all of which point to the dangers of holding leveraged ETFs long term.

The charts below shows six distinct horizontal markets with varying levels of volatility. In the bottom right box are the returns of the index, the 2x ETF and the 3x ETF. As you can see, market environments with higher volatility that continue over time have the largest negative impact on leveraged ETFs.

While it is true that leveraged ETFs do erode in value during market environments with high volatility and a horizontal direction, the amount is relatively small over a 25-day time frame. If the horizontal high-volatility market environment continued for a substantial amount of time — say holding longer than a year — then we would see a significantly larger erosion in share value.

Leveraged ETFs Underperformed in 2008

Between its inception date (in June 2006) and October 2015, the ProShares Ultra S&P 500 (SSO ), the 2x S&P 500 ETF, underperformed the S&P 500 most of the time. However, to date, the overall increase in value is about the same at 57%.

Leveraged ETFs are designed to be highly sensitive to daily changes in the underlying index. So when the index plummets, like in 2008, the drawdowns of the ETF (if bullish like SSO) will be substantial. For example, from January to December 2008 the drawdown was 67.6%.

For investors in leveraged ETFs, drawdowns of this size mean that getting back to “par value” will be extremely difficult. Even though SSO was gaining 2x the S&P 500 after this drawdown, it took a long while, about five years, before it was able to make up its losses.

The Fees Will Drag Down Overall Investment Value

All ETFs charge management fees for providing the service of constructing and managing the ETF’s day-to-day operations. Leveraged products generally charge more than regular ETFs. A good rule of thumb is the more complicated the ETF, the larger the fee.

The longer an investor holds an ETF, the more fees he or she will have to pay. However, compared to mutual funds, ETFs (even leveraged ones), still offer great value when it comes to fees.

Extremely Long Holding Times Can Destroy Value

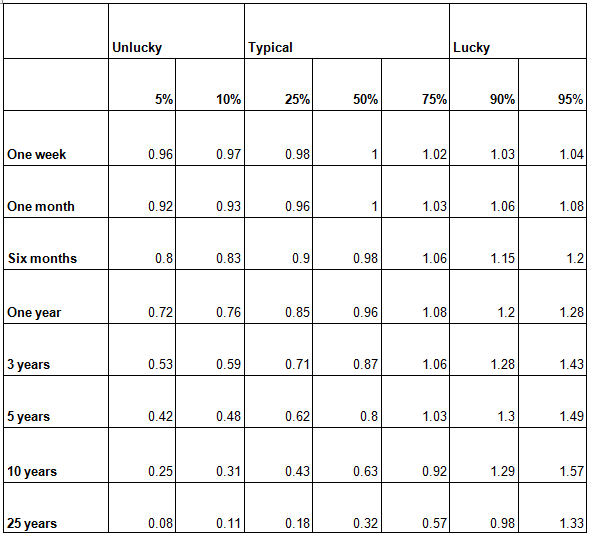

Using the classic example of “random walk”-generated stock data, we can estimate the erosion of value of a leveraged ETF on a portfolio over extremely long periods of time. For this study we randomly generated 25 years of “stock index return data” and broke it into cohorts that range between extremely lucky ETF investors, typical investors, and extremely unlucky ETF investors.

By looking at the “typical” columns we can clearly see that holding leveraged ETFs in a “random walk” environment over the long term destroys asset value. By using this type of analysis, it becomes clear why the names “leveraged decay” and “volatility drag” have survived to describe the long-term holding of leveraged ETFs.

The Bottom Line

Leveraged ETFs are best used for investments with a clearly defined directional environment and with holding periods of less than one year. The chance for a massive drawdown, and the subsequent inability to get out of the drawdown, is simply too large of a risk for a long-term retail investor.

Leveraged ETFs should be used in trading situations where there is a strong conviction in market direction and with a clearly defined trading strategy. Simply buying and holding leveraged ETFs in an uncertain market environment will not benefit the long-term investor and will negatively impact their returns.

Image courtesy of cooldesign at FreeDigitalPhotos.net