All that glamour isn’t growth — this was a pervasive theme in a Research Affiliates webinar entitled Growth vs Glamour: Rethinking What Drives Equity Returns. Rob Arnott, founder and chairman of Research Affiliates, along with Brent Leadbetter, partner at the firm, outlined the shift in how investors should categorize and weight the growth factor. Ultimately, the session served as a challenge to the industry’s long-standing reliance on valuation multiples as a means of identifying growth. Instead, Arnott and Leadbetter cited a fundamental growth strategy, anchored in observed economic data from years past as a more effective growth indicator.

Key Takeaways

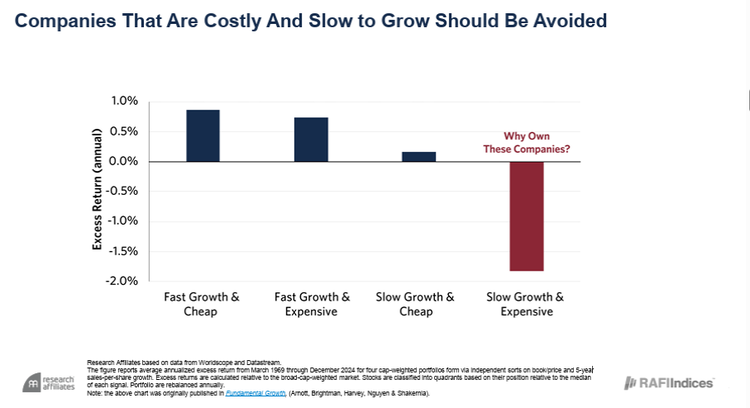

- “Glamour” stocks — those that are expensive but exhibit slow actual growth — trailed the broad market by 2% per annum compounded over a 57-year period.

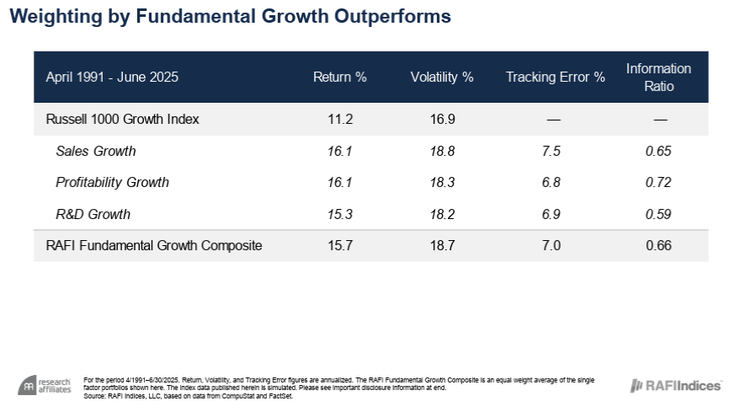

- The fundamental growth strategy selects and weights companies based on the actual dollar magnitude of their sales, profitability, and R&D spending rather than relying on high valuation multiples.

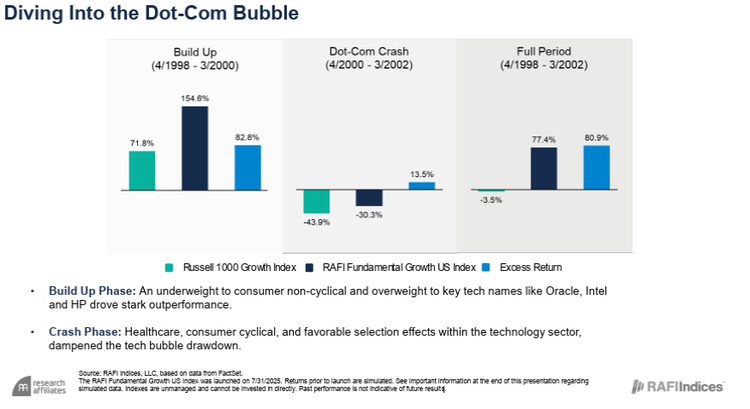

- During the four-year span of the dot-com bubble and subsequent crash, the RAFI fundamental growth strategy would have yielded a 77%, return while the Russell Growth index finished in negative territory.

See More: Rob Arnott on Market Disconnections, Growth & More

Expensive Is Not Growth

For decades, the investment community has largely relied on traditional finance academia from the Fama-French model. In that logic, a stock falls into one of two categories: It exhibits traits that are conducive to value (cheap relative to its fundamentals) or growth (expensive relative to its underlying value). Arnott argues that this “binary duality” has flaws.

“Expensive is expensive. Expensive isn’t growth,” Arnott noted. “It’s presumptively high future growth if the market is efficient, but if it’s doing all of that, you’re not going to get a premium return anyway, because it’s already in the price.”

To counter the traditional value versus growth argument, Research Affiliates suggests looking at the two factors through a different lens. Two dimensions stand out as particularly important: growth versus slow growth, and cheap versus expensive. Their research, which draws from data all the way back to 1969, found that the “slow growth/expensive” bucket — referred to as the “glamour” bucket — trailed the broad market by 2% per annum, compounded over 57 years.

“Slow growth and expensive… is to be avoided,” Arnott emphasized.

Summarily, Research Affiliates cited that past growth is a far more reliable predictor of future growth compared to high valuation multiples. The firm’s strategy selects and weights companies based on three key metrics of growth: sales, profitability, and research & development (R&D).

As opposed to strictly relying on market capitalization, Research Affiliates equally weights this triage of signals and focuses on the dollar magnitude of said growth. This targets companies providing the requisite horsepower to move the U.S. economy.

“If you want to weight a growth portfolio sensibly, you want to weight it by the dollar magnitude of the growth,” Arnott said, citing data from the past 56 years to support this assertion. “Not by the market cap, and not proportional to the market valuation multiples.”

A Differentiated Growth Index

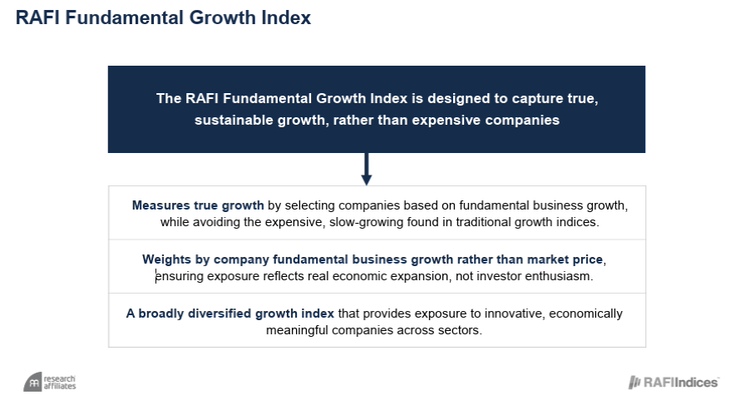

To highlight this strategy at work, Research Affiliates explained the mechanics of the RAFI Fundamental Growth Index. Ultimately, the index aims to provide exposure to companies exhibiting true growth as opposed to simply being expensive.

A vivid example of this strategy at work is the Magnificent Seven. The RAFI index is currently overweight Alphabet and Meta due to their immense trailing growth. However, it notably excludes other Magnificent Seven peers, like Amazon and Microsoft.

“Microsoft has had sales growth that’s very nice, but none of those numbers is in the top quartile,” Arnott said. “Past growth is a far more reliable predictor of future growth than high multiples are.”

The strategy’s resilience proved its mettle when examining the Dot-Com era. More specifically, during the last two years of the bubble (1998–1999), the fundamental growth strategy would have outperformed the Russell Growth index significantly. More importantly, during the subsequent crash, it provided a defensive cushion for downside protection. Over the full four-year span of the bubble and subsequent burst, the Russell Growth index gave investors a negative return. In stark contrast, the RAFI fundamental growth strategy would have yielded a 77% return.

Balancing Value and Growth

The webinar taught the audience that growth doesn’t exist in a portfolio vacuum. Arnott advocated for value, noting it is currently in its bottom decile of relative cheapness. Conversely, speaking to investors who want or need growth exposure, Arnott noted that the traditional path is fraught with overvaluation risk.

“To the extent that you want growth in your portfolio, you can do way better,” Arnott concluded. “Selecting by growth, weighting by growth gives you a better experience than simply weighting by market cap.”

In the 24-hour financial news cycle, it’s easy for investors to get caught up in the hype. Research Affiliates have stripped away the glamour of narrative-driven stories and focused on the objective reality given through financial statements. In doing so, they believe they have unlocked a more disciplined, and ultimately more profitable, way to harness growth.

For more information on this investment premise, read Outgrowing Glamour: A Fundamental Approach to Growth Investing.

Originally published on Advisor Perspectives

For more news, information, and strategy, visit ETFDB.