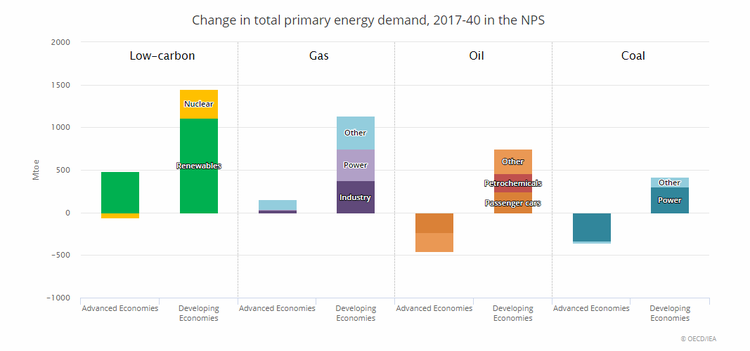

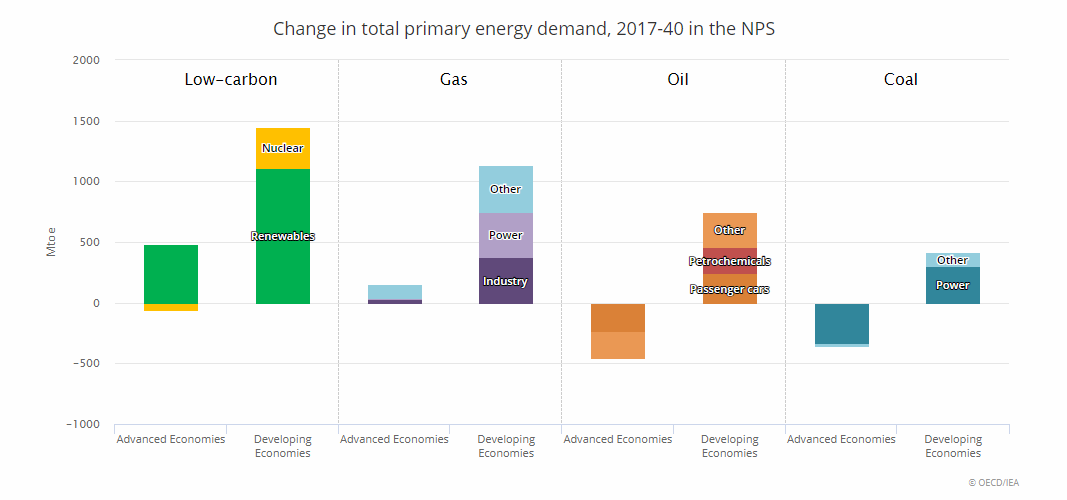

Instead, energy demand growth will be driven by developing economies as shown in the chart below from the International Energy Agency’s (IEA) World Energy Outlook 2018. In the New Policies Scenario (NPS), which factors in announced energy policy plans and targets, energy demand is forecasted to grow by over 25% through 2040, with India leading the way in demand growth. Increased demand is driven by higher incomes and population expansion to the tune of 1.7 billion people. The IEA notes that the growth in energy demand would be around twice as much if not for ongoing progress with energy efficiency. As shown, renewables and natural gas are expected to see increased demand in both advanced and developing economies. Decreasing oil demand in advanced economies is expected to be more than offset by growth from developing economies, driven by rising demand from petrochemicals, aviation, and trucking. Growing demand for energy overseas, particularly in developing countries, will support growing exports of crude, liquified natural gas, petroleum products, and natural gas liquids from the US and Canada.

Source: International Energy Agency, World Energy Outlook 2018

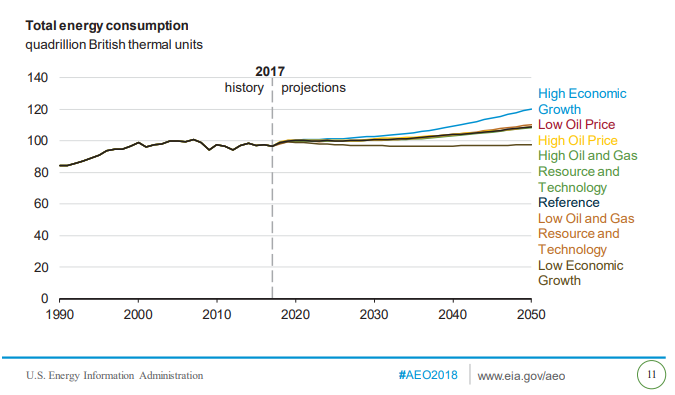

In the scenario above, both renewables and hydrocarbons are expected to see demand growth through 2040. Renewable energy can be viewed as a long-term threat to businesses that are based around hydrocarbons, including MLPs and midstream companies. However, we would note that switching energy sources is a long process. Coal consumption in the US peaked in 2007, barely more than a decade ago. In 2017, coal consumption in the US was down 36% from its 2007 peak, but coal still accounted for 30% of US electricity generation that year. Globally, coal demand is expected to have increased for the second-straight year in 2018, and the IEA forecasts that demand will remain stable over the next five years, even with climate policy at the forefront for governments. If coal is any indication, oil likely has a long runway of staying power (pun intended).

The US is poised to play a dominant role as a global energy supplier.

In 2018, the US became the world’s largest oil producer, and the US has been the world’s largest natural gas producer since 2009. For the first time since the 1940s, the US was a net exporter of crude and refined products for one week last year – a feat that would have been nearly unimaginable 15 years ago. Even with the significant production growth in recent years, abundant resources remain untapped. US oil and natural gas proved reserves reached record levels in 2017. With this resource base and technical expertise, the US is expected to lead global production growth for oil and natural gas. Specifically, under the NPS of the World Energy Outlook 2018, the IEA has forecasted that the US will account for almost three-quarters of the total increase in global oil output to 2025 and 40% of the global increase in natural gas production to 2025. As production increases, energy exports will also rise, and energy infrastructure (pipelines, terminals, processing capacity) will be needed to facilitate both growing production and exports.

Lower oil prices represent a risk to production, and a number of weeks with WTI oil prices in the $40 per barrel range could temporarily interrupt the growth trajectory if producers begin to slow their activity. Since a significant amount of natural gas production comes from oil-focused wells (gas from these wells is called associated gas), lower oil prices can also impact natural gas production. The remedy for low oil prices is low oil prices, as some production will rationalize to bring supply and demand back into balance. Production cuts from OPEC and non-OPEC allies, including Russia, which came into effect on January 1, 2019, may help support prices and prevent a prolonged period with WTI oil prices in the $40s. WTI had recovered to over $48 per barrel as of January 7.

Beyond fundamentals, MLPs and midstream have cleaned house in many ways.

As we discussed in our 2019 outlook video, the midstream space is making strides to attract new investors. Many MLPs have eliminated their incentive distribution rights (IDRs), responding to investor disdain for them. MLPs and midstream companies have improved their leverage metrics and shifted more towards self-funding their equity instead of tapping equity capital markets. MLPs are better able to afford their distributions as evidenced by higher coverage ratios (read more). Both corporations and MLPs are even talking about buybacks, with Enterprise Products Partners (EPD) repurchasing 1.2 million units ($30.8 million) in December and MPLX (MPLX) mentioning buybacks as a possibility at its December analyst day if the market is not rewarding distribution growth. As of its most recent 10-Q from 3Q18, Kinder Morgan (KMI) had repurchased $500 million in shares under its $2 billion buyback program that began in December 2017. Additionally, the wave of MLP/midstream consolidations and restructuring transactions should be largely behind us, removing some of the uncertainty that has been an overhang on the space (read more).

The process of MLPs and midstream companies righting the ship has not been easy. Painful distribution cuts and the tax implications of consolidation transactions have been frustrating for investors. In other cases, the moderation of distribution growth to pursue self-funding equity has perhaps disappointed investors that had become accustomed to greater growth rates. While fundamentals have been strong in terms of production growth, there has been a disconnect between fundamentals and midstream equity performance in part because of the noise in the space and this ongoing, painful transitional phase. It feels like midstream is getting closer to the conclusion of this “cleaning house” phase, which could be a catalyst for generating more interest. Admittedly, recent oil volatility and WTI crude in the high $40s may act as a near-term headwind to generating interest in energy equities broadly, including in MLPs and midstream.

Bottom line

The high-level thesis for investing in MLPs and midstream can be summed up as follows: 1) the world is going to need more oil and natural gas, 2) the US (and Canada to a lesser extent) will play a major role in meeting that demand with growing energy production and exports, 3) connecting supply with demand is going to require energy infrastructure, and 4) MLPs and midstream companies will be able to collect fees, often under long-term contracts with built-in inflation protection, for the utilization of those assets and will generate cash flows for their investors. This fairly simple story has been complicated with lots of noise, but as the space cleans house, that noise should start to subside.

{kind=link}

{kind=link}