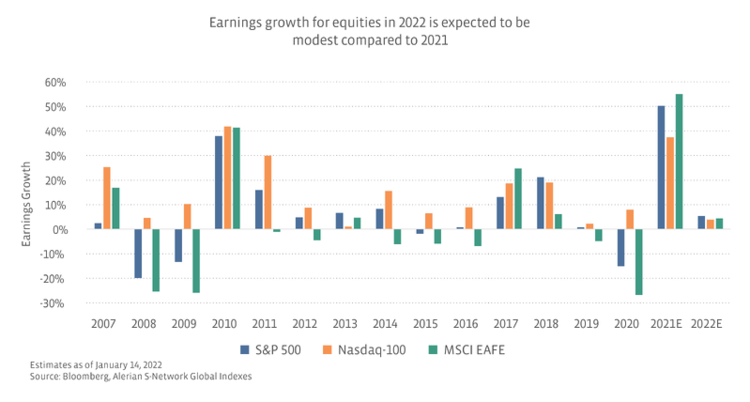

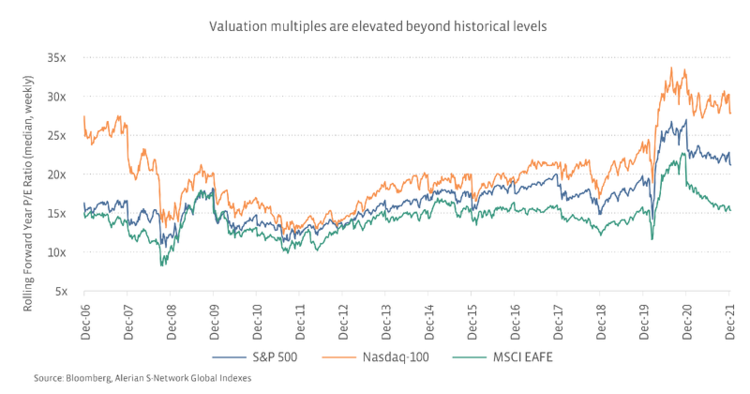

Why be cautious in 2022? Earnings growth likely less supportive.Valuations (measured by forward P/E ratios) of broad equities have been trading above historical levels, and higher equity prices have been supported by strong corporate earnings. Although earnings growth is expected to be positive in 2022, the rate of expected growth is very modest compared to 2021 when earnings staged a strong recovery after a challenging 2020. Much of the strength in 2021 corporate earnings can be attributed to large technology companies which benefited from both the acceleration of the digital transformation and strong consumer spending. (Information technology is the largest sector in both the S&P 500 and the Nasdaq-100 with a 29% and 56% portfolio weighting, respectively as of year-end 2021.)

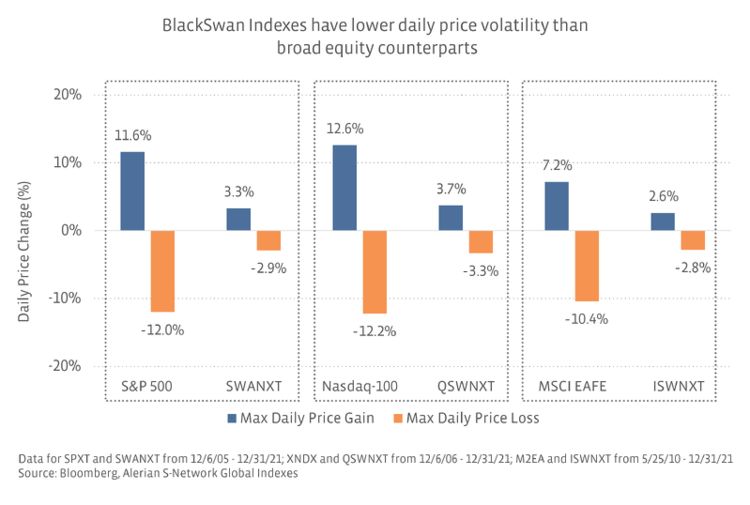

Additionally, strong consumer spending will likely be less of a growth driver for 2022. Consumer strength in 2021 was propped up by several rounds of stimulus checks and COVID-19 unemployment benefits. Consumers are now dealing with high levels of inflation from supply chain disruptions, which show up as higher prices. More people may be encouraged to wait out higher prices and longer shipping times from supply chain disruptions by either rethinking or delaying purchases.Recent equity strength may be driving misalignment between risk appetite and risk tolerance.In response to inflation, the Fed has started to wind down pandemic stimulus to stop the economy from overheating. Previously, the Fed referred to inflation as “transitory.” But in recent meetings, they have shifted their tone by saying that controlling inflation is their “most important task.” The Fed has already commenced scaling down asset purchases and expects to raise interest rates three (possibly four) times in 2022, which is expected to start as early as March. Generally, higher interest rates are bad for stocks. First of all, higher interest rates will increase the cost of borrowing for corporations, which can reduce earnings growth. Higher interest rates can also decrease the attractiveness of equities compared to bonds (e.g., less attractive yields). Additionally, companies are often valued on their future cash flows, which are discounted by interest rates—discounting by a higher interest rate will lead to a lower perceived value.The Fed has been addressing stretched valuations since its May 2021 Financial Stability Report. In its November 2021 report, it emphasized again that “asset prices may be vulnerable to significant declines should risk appetite fall.” With the possibility of significant price declines, all three BlackSwan Indexes provide a useful strategy for investors to better align risk appetite with risk tolerance by participating in equity gains without risking significant portfolio losses.

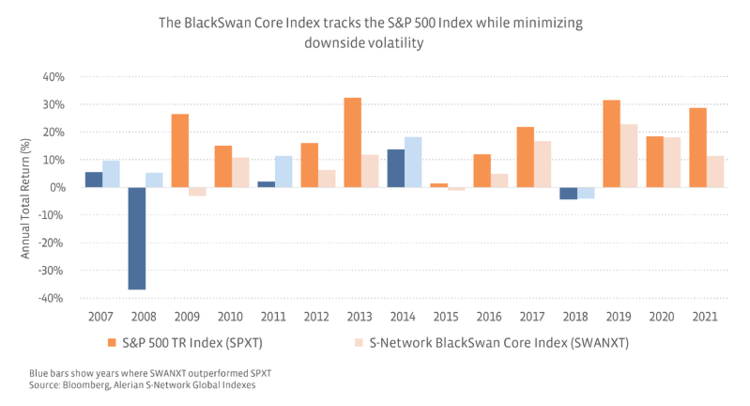

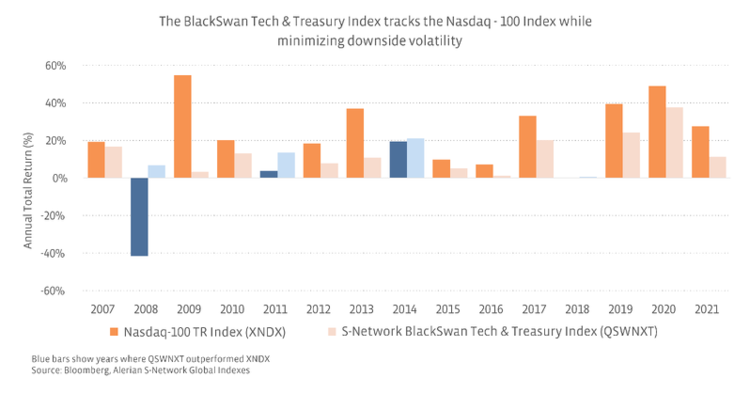

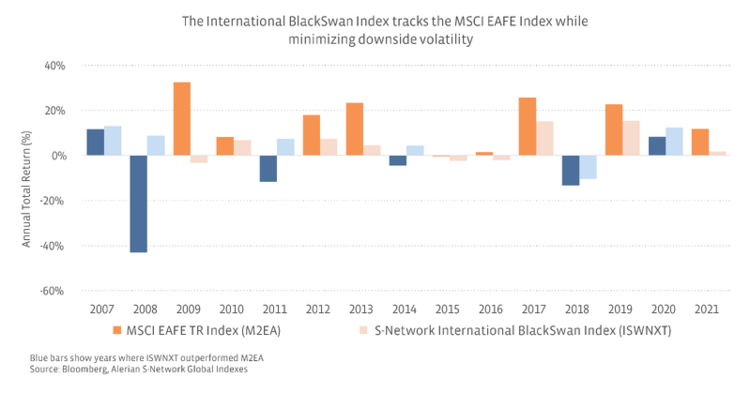

Investors can lessen the fear of short-term price fluctuations while still participating in equity upside.Some investors may have portfolios which cannot afford short-term price fluctuations, and others may not want the stress of watching their investment value shift drastically from day-to-day. In addition to minimizing long-term downside risk, the BlackSwan indexes can also help prevent large short-term price fluctuations, which may ease some portfolio anxiety in an uncertain market environment.

Bottom Line: The market is already difficult to predict, but Black Swan events like the COVID-19 pandemic are almost impossible to foresee and can poke holes in an otherwise sound investment strategy. Risk-averse investors and investors closer to the distribution stage of their portfolios may consider the Swan family of indexes as a method to participate in equity appreciation while reducing downside volatility compared to a direct equity allocation.The SWANXT Index is the underlying index for the Amplify BlackSwan Growth and Treasury Core ETF (SWAN).The ISWNXT Index is the underlying index for the Amplify BlackSwan ISWN ETF (ISWN).The QSWNXT Index is the underlying index for the Amplify BlackSwan Tech & Treasury ETF (QSWN).