Summary //

- Even with total US auto sales declining in 2020, several electric vehicle companies reported record high deliveries last year.

- The long-term outlook for EVs shows significant growth for the sector over the next two decades driven by supportive government policy and acceleration of investment in the space, among other things.

- Given the long-term importance of EVs to the energy transition, EV manufacturers are a critical component of an alternative energy allocation.

In a year filled with market turmoil, alternative energy stood out as a bright spot in 2020. The Ardour Global Alternative Energy Extra-Liquid Index (AGIXL) finished the year up 120.3% on a total-return basis, significantly outpacing the broader market. While some of these gains can be attributed to other segments of the alternative energy space, particularly solar, electric vehicle (EV) manufacturers led the charge last year. EV manufacturers BYD (1211), Tesla (TSLA) and Nio (NIO) saw staggering gains of 423.6%, 743.4%, and 1,112.4% in 2020, respectively. Despite this significant run-up last year, strong operational reports from EV companies in early 2021 indicate that there could be more left in the tank. Today’s piece examines updates from EV manufacturers and how the outlook for EVs could drive further alternative energy outperformance. (Puns intended throughout).

EV adoption continues to rise despite COVID-19 impacts.

With lockdown measures in place and many companies moving to a work-from-home policy during 2020, car purchases were likely not front of mind for most people. Overall, 2020 US auto sales are expected to have declined roughly 15% year-over-year to approximately 14.5 million, representing their lowest level since 2012. However, this broad decline has not slowed down pure-play EV manufacturers that continue to report record high deliveries. TSLA recently announced that full-year 2020 deliveries totaled 499,550, effectively matching their guidance of 500,000 and representing a nearly 36% year-over-year increase. Vehicle production for the year was slightly higher at 509,737. Chinese EV manufacturer NIO set new all-time highs for vehicle deliveries for December and 4Q20, with total annual deliveries of 43,728 representing a 112.6% year-over-year increase. While this is in part a reflection of improved production capabilities by EV manufacturers, substantial growth figures also demonstrate resilient demand for EVs even as broader auto sales fell. Additionally, more traditional automakers continue to push into the EV market, underscoring the long-term viability of the space. As an example, General Motors (GM) shares set a new all-time high on January 12 after the company unveiled its BrightDrop business, which includes a portfolio of EVs and other zero-emission products to aid companies in the electrification of first-to-last mile delivery. Though traditional auto manufacturers are moving in to the EV space, existing EV players’ established brands and demonstrated ability to produce EVs at scale represents an advantage.

What’s in store for EVs going forward?

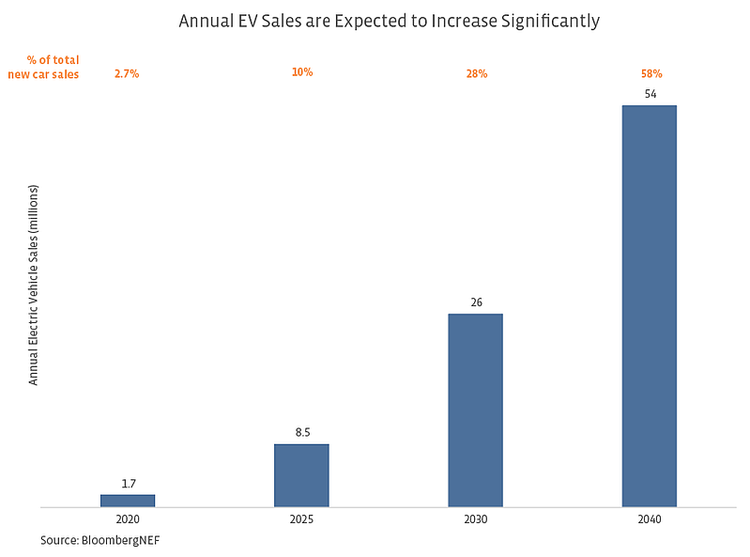

Even after a banner year in 2020, the long-term outlook for EVs shows no sign of pumping the brakes. BloombergNEF’s Electric Vehicle Outlook 2020 helps frame the growth potential for the EV market over the next two decades. This report estimates that passenger EV sales will increase by 18.9% annually from 2020 through 2040, as seen in the chart below. Over that same time period, the sales market share of EVs is expected to rise from 2.7% to 58%, driven particularly by China and Europe. Most of the growth in EV adoption is expected to occur within the next decade, however, with the global EV fleet estimated to increase by 13.6x by 2030; although, it’s worth mentioning that starting from a lower base drives these growth figures higher. Rapid adoption of EVs should be propelled by improving battery technology, favorable economics for buyers, and an acceleration in investment in EVs by automakers. Innovations in battery technology by EV companies also have positive implications for the rest of the alternative energy space, as discussed in Alerian’s November 2020 white paper (read more).

Government incentives will also play a major role in this expected EV growth. Several countries, including the UK, France, and Norway, have established bans on the sale of internal combustion vehicles in the coming decades, with the UK recently moving up its ban on new diesel/petrol cars and vans to 2030 compared to its original target of 2040. The EU COVID-19 stimulus package contains several measures designed to help countries increase EV adoption, including the installation of two million electric and hydrogen charging stations by 2025 and €20 billion to support clean public transit. Notably, EV costs in the EU are expected to be competitive with that of traditional petrol vehicles by next year. In the US, California will phase out the sale of gas-powered vehicles by 2035 and will require all medium- and heavy-duty trucks to be zero-emission by 2045, in line with the state’s 2045 net-zero target. Policies from the new administration in the US could also represent a catalyst for EVs. President-elect Biden has proposed working with cities and states to install more than half a million public charging stations over the next decade and restoring tax credits for EV purchases. While growth in EV adoption would likely occur regardless of these policies, supportive initiatives from governments across the world will help accelerate the push towards net-zero transportation.

EV manufacturers an important component of the alternative energy universe.

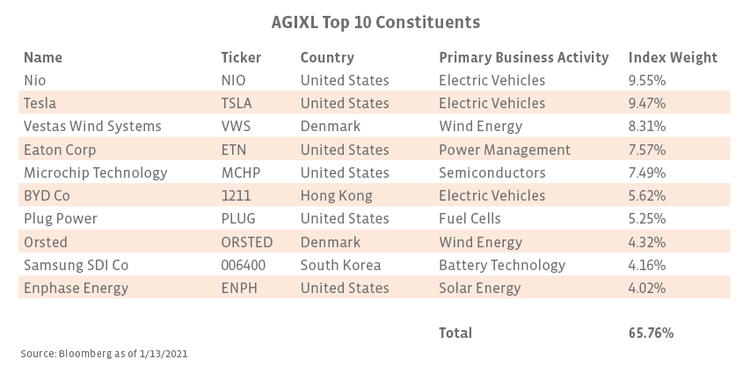

The Ardour Global Alternative Energy Indexes were the first indexes to provide globally-inclusive, alternative energy exposure. AGIXL represents an investable subset of the broader alternative energy universe. The index has constituents across several clean energy subsectors, including wind and solar energy players, semiconductor manufacturers, and, importantly, electric vehicle manufacturers. Given the long-term importance of EVs to the clean energy transition, these companies represent a critical component of the alternative energy universe. As of January 13, AGIXL’s two largest constituents, which accounted for 19.0% of the index by weighting, were NIO and TSLA. When including BYD, EVs account for nearly one-fourth of AGIXL by weighting. This leaves the index well positioned to capture upside from the trends in EVs as well as the broader growth in clean energy.

Bottom Line

As more governments and corporations aspire to transition toward a carbon-neutral world, EVs are poised to become more and more common. Given existing equity price momentum, constructive operational reports, and a supportive long-term outlook, EVs present an opportunity for investors to add ESG-friendly growth to their portfolios. AGIXL reflects the growth opportunity in EVs while providing broader exposure to the energy transition through diversified clean energy exposure.

AGIXL is the underlying index for the VanEck Vectors Low Carbon Energy ETF (SMOG).