Many have also asked how we calculate distribution growth. Here’s the scoop:

First, we examine the individual distribution growth rates for each index constituent on a quarterly basis. Those constituent-level growth rates are then multiplied by each constituent’s weight in the index. Those weighted values are then combined to give the overall weighted quarterly distribution growth for the index. That growth rate is then set to its own index. We then calculate the annual distribution growth by comparing the sum of the index values from the four quarters in each year vs the sum of the index values from the four quarters of the previous year.

The process is a little bit confusing, or at least, it was a little confusing to me before our data team explained it to me in terms my 7-year-old goddaughter could understand. A common misconception is that we simply take the weighted distribution growth of each quarter and sum the four quarterly growth numbers to arrive at the annual number. Don’t let yourself be tripped up by this. In 2015, the distribution growth numbers by quarter for the AMZ were 1.1% (Q1), 0.9% (Q2), 1.6% (Q3), and 1.0% (Q4). These figures sum to 4.6% not 5.1%. The reason for the discrepancy is that, as I touched on above, the annual distribution growth in a given year is based on a comparison to the previous year.

Think of it like this:

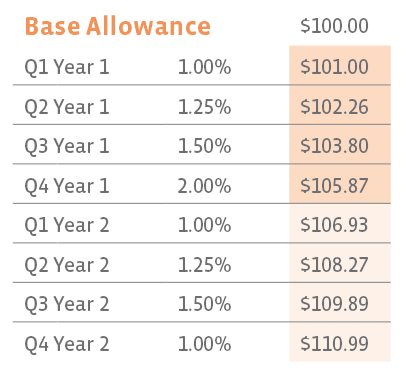

You’re a no-nonsense parent that decides to give your child raises on his allowance each quarter based on merit.

The first payment is a freebie which you give to your child for Christmas. It’s $100 big ones. All raises will be based off this $100 base value. In Q1 of the first year, you give your child a 1% raise. Q2 a 1.25% raise and so on as shown in the chart below:

To calculate the percentage of your child’s allowance growth, you’d add up the total amount he received in year 1, $412.93, and the total amount he received in year 2, $436.08. You’d then divide the total from year 2 by the total from year 1 and subtract 1. ($436.08/$412.93) – 1 = 5.6%. This would give you the annual allowance growth.

This is almost exactly how it works with the distribution growth calculation, with the key difference being that the figures in our equation are not dollars, but indexed growth numbers.

One other frequently confused item is which data we’re applying to each quarter. When Alerian calculates the distribution growth rate for 4Q15, we use the distributions announced and paid in 1Q16. We do it this way because it best reflects the performance of the MLP/business/assets during the period we reference. The distributions paid in 1Q16 are a result of the company’s performance during 4Q15. Some investors get mixed up because they use the period in which the distribution was paid. Please don’t let this be a stumbling block for you when you’re trying to double check our numbers.

As always, if you have further questions, email me at [email protected]. I’m always looking for new EFs.

{kind=link}

{kind=link}