Let’s pretend that PresJP announced a $0.55/unit distribution for Q3 2015. Before gaining a real understanding of this, I thought you took $0.55, divided it by two, and called it a day. 50/50 split, right? Seemed a little unfair that the LP unitholders had to give up half their distributions, but, agreements are agreements. This is not correct! Remember, the LP unitholders will always get the full amount of the distribution declared.

Grab my hand and I’ll walk you through this line by line to help you understand what will be owed to the GP. As we get started, compare these tiers to the progressive tax system (explained in more detail here). Each “section” will be treated differently.

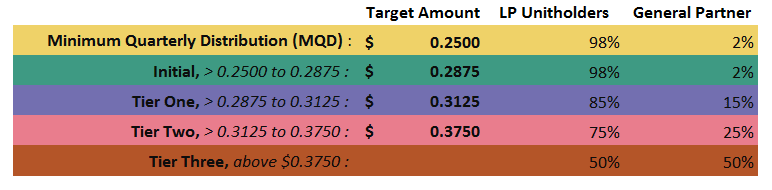

Yellow Section

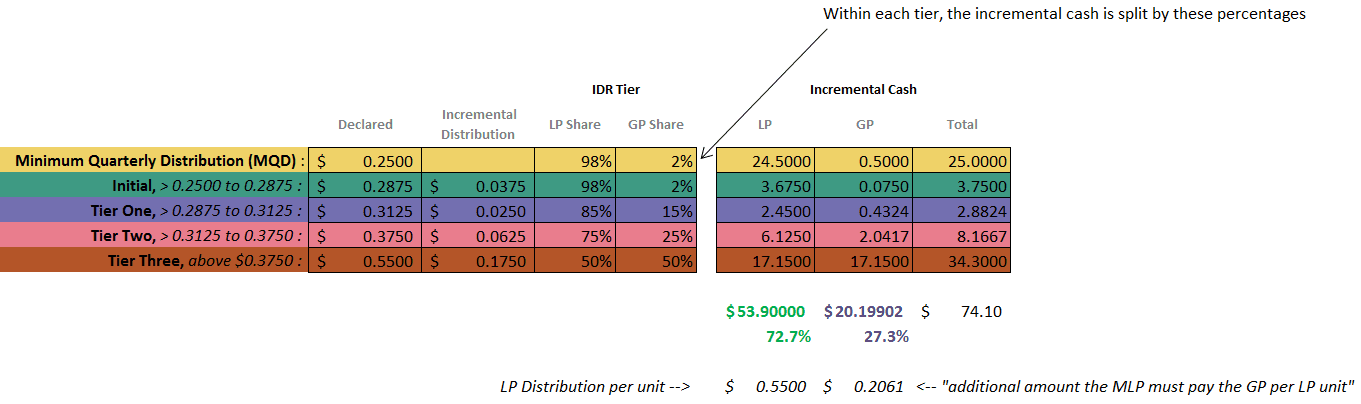

This section is pretty straightforward. There’s no fancy business occurring here. The first $0.25 is simply multiplied by the 100 units outstanding to get $25 in total distributions. 98% of the $25, $24.50, goes to the LP unitholders, and the other 2%, $0.50, goes to the GP. IDRs haven’t kicked in yet.

Green Section

This section also works out as you might expect because IDRs still haven’t started yet. You take the 2nd sliver of distribution, $0.0375, found by subtracting the yellow target amount from the green target amount, and multiplying it by 100 to get $3.750. $3.675 goes to LP unitholders and $0.075 goes to the GP.

Purple Section

This is where things get real. IDRs are now in play. To determine what portion of the distribution paid will be subject to IDRs, start by subtracting the green section target amount from the purple section target amount.

$0.3125 – $0.2875 = $0.0250

Multiply this by 100 for the total amount paid at this level ($2.50), then multiply $2.50 by 98% to figure out the cash owed to the LP unitholders. The answer is $2.45. (The remaining $0.05 goes to the GP because of their 2% ownership interest.)

At this level, only 85% of this tier’s cash should go to the LP, so the MLP has to pay additional cash to the GP (this is the IDR payment). To determine how much more, we have to figure out how much should be paid.

Backing into the math, divide $2.45 by 85% to get $2.8824. Since we already know what the LP unitholders get, subtract that amount ($2.45) from the total ($2.8824) and you’ll get $0.4324. This $0.4324 (or 15% of the total incremental distributions paid) is what goes to the GP. Note: This $0.4324 includes the $0.05 from the 2% GP interest, so the “IDR portion” is $0.4324-$0.05 = $0.3824.

Pink Section

Same ideas as described in the purple section, except the GP take at this level is 25%, so I’ll cut to the chase with the math only:

- Subtract the purple section target amount from the pink section target amount, $0.3750-$0.3125 = $0.0625

- $0.0625 × 100 = $6.25

- $6.25 × 98% = $6.125 owed to LP unitholders

- $6.125 ÷ 75% = $8.1667

- $8.1667 – $6.125 = $2.0417 owed to GP

Brown Section

Same business as the purple and pink sections, except the GP take at this level is 50%. Here is the math:

- Subtract the pink section target amount from the declared distribution, $0.55-$0.3750 = $0.1750

- $0.1750 × 100 = $17.50

- $17.50 × 98% = $17.15 owed to LP unitholders

- $17.15 ÷ 50% = $34.30

- $34.30 – $17.15 = $17.15 owed to GP

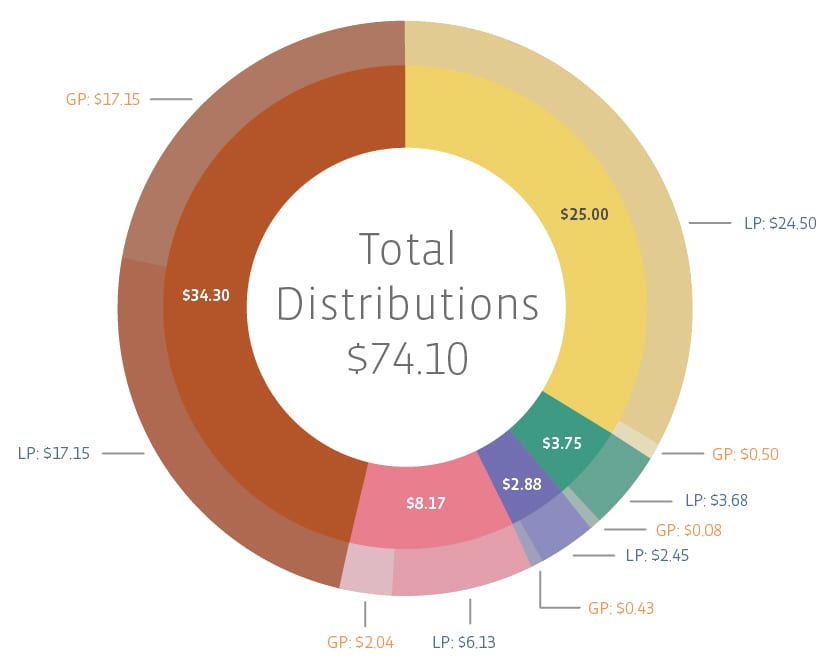

So what amount goes to the LP unitholders and what amount goes to the GP? Add everything up. In total, LP unitholders would receive $53.90 and the GP would receive $20.20 in this example. The total cash paid out would be $74.10 and the GP would end up receiving 27.3% of the pie – not 50%. I know. I was shocked too.

In case you still aren’t convinced that LP unitholders always get the full amount declared, if you take the $53.90 and divide it by 98 units, you get $0.55/unit, which is the declared distribution. Effectively, this also means the GP receives $0.2061 per LP unit ($20.20 divided by 98 units); this is not a real term, but may help you conceptualize that when $0.55/unit is paid to LP unitholders, an additional $0.2061 per LP unit must be paid to the GP. In a case where an MLP did not have a GP, this $0.2061 is extra cash flow that could have been paid to LPs.

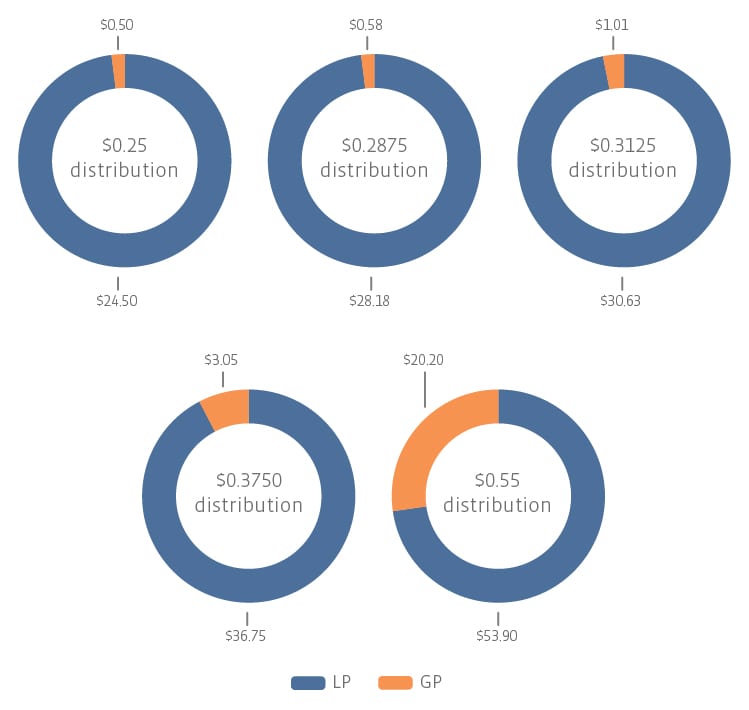

Additionally, here is a peek at how the splits look at each tier. For example, if PresJP hadn’t yet reached Tier Three, you can cover up the bottom tier to see that at Tier Two, if the dividend were $0.3750/unit, the LP would receive 92.3% of the pie, a significantly larger piece than in Tier Three. Speaking of pies, here are a few that show the splits at each level of distribution listed in the chart above and discussed in our example.

Hopefully, this illustration cleared up any confusion you’ve had over IDRs. If you have any additional questions or are an expert in geometry and would like to help me clear up my sketchy past with proofs, please email me at [email protected].

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}