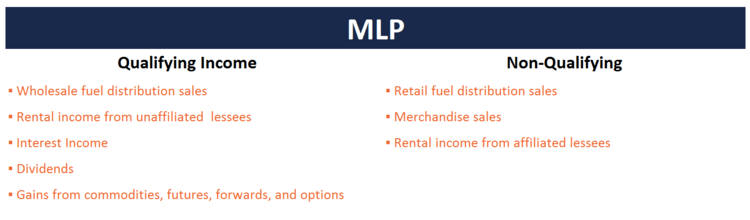

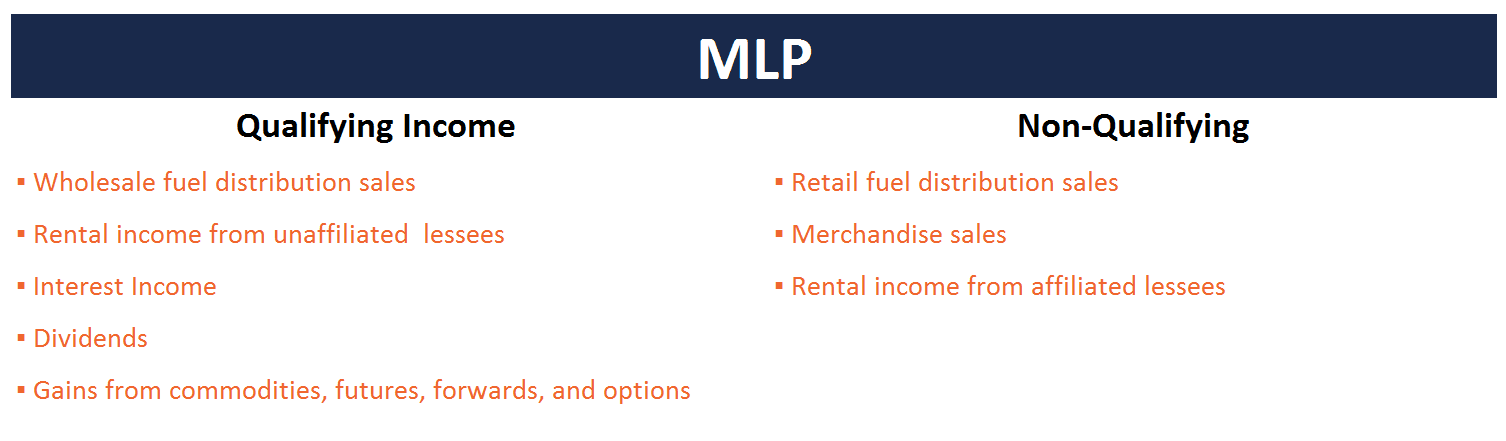

When a c-store is purchased by an MLP, there are portions of the associated income that are qualifying, and portions that are not.

(Adapted from slide 31 of this SUN presentation.)

MLPs can separate out the non-qualifying income by leasing the stores they own to a third party or an affiliate company who will collect the profits from retail fuel and merchandise sales. If your neighbor enjoyed running gas stations and decided to lease and operate a store from GLP, he would be considered a third party. An affiliate company would be an entity like Stripes LLC, if SUN were the lessor. Some MLPs place the non-qualifying income in a corporate subsidiary and pay taxes therein. For example, SUN has a corporate subsidiary called Susser Petroleum Property Company LLC (PropCo).

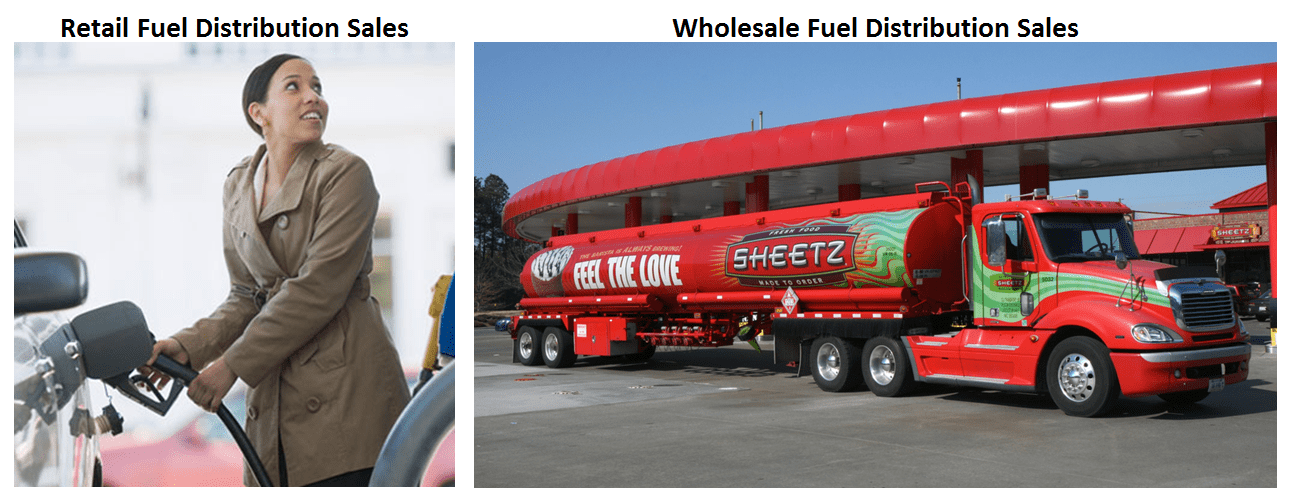

When an MLP owns a gas station, it can function as the wholesale fuel distributor. So while the MLP can’t sell gas to the gal filling up her Accord, it can sell to the convenience store itself (and it doesn’t hurt when one of your biggest customers is yourself).

In addition to this, MLPs can generate qualifying income from a host of other sources reflected in the chart, such as rental income when the lessee is a third party and dividends when the gas station is owned by a corporate subsidiary.

At first glance, MLPs as c-store owners may not seem logical. However, upon further inspection, MLPs owning gas stations can be a great “combo” of wise business structure and tax planning.

{kind=link}

{kind=link}

{kind=link}