While WTI is a poor global benchmark, it is an important tool for domestic energy companies. Exploration and production companies may use WTI and related derivative instruments to hedge their oil production. Refiners may also use WTI futures and derivative instruments to manage risk and hedge the price exposure of their oil inventories. When hedging domestic production or crude inventories, WTI is a better fit than Brent. The WTI Cushing contract also provides liquidity and market depth, with almost 1.2 million contracts traded each day and more than 2 million contracts in open interest.

When it comes to growing exports of crude from the US, the WTI contract takes a backseat to coastal prices, which are what matter for exports. Specifically, market observers typically focus on the price of crude at Houston and St. James, Louisiana. Two new crude futures contracts priced in Houston recently launched with physical delivery (the existing Argus WTI Houston swap is financially settled). On October 22, the Intercontinental Exchange (ICE) launched a new contract for Permian WTI crude futures, and CME Group launched a new WTI Houston futures contract last Monday. The ICE contract provides price discovery at Magellan’s (MMP) East Houston terminal, and the CME Group’s contract provides price discovery at Enterprise’s (EPD) Houston terminals.

The two contracts’ different delivery points and different specifications provide alternatives, as discussed in this Argus article, but they also probably divide volumes and liquidity among financial players. ICE Permian WTI Houston saw ~445 contracts sold on its first trading day, while the CME Group’s WTI Houston traded 26 contracts on its first trading day. It’s likely that neither Houston contract will rival WTI trading volumes any time soon, but volumes will probably grow over time. Additionally, WTI Cushing will probably continue to offer more liquidity along the futures curve, which is helpful for producers trying to hedge production in future years.

Let’s get physical – Cushing infrastructure is tough to beat.

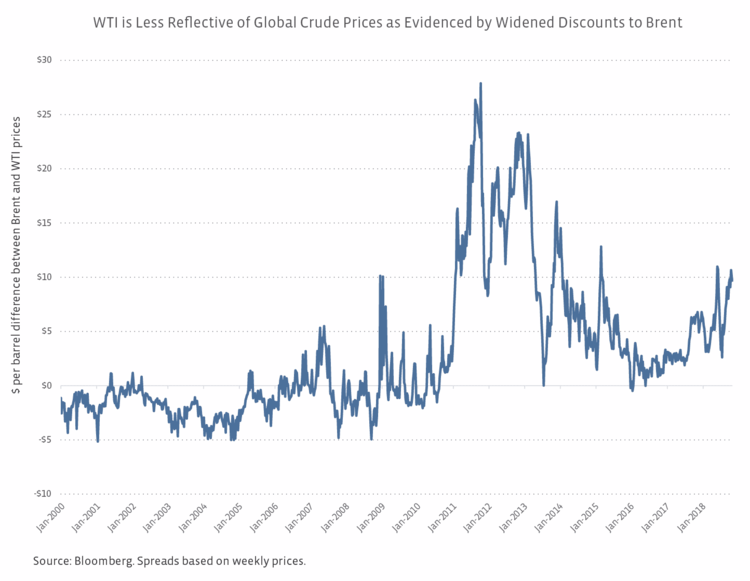

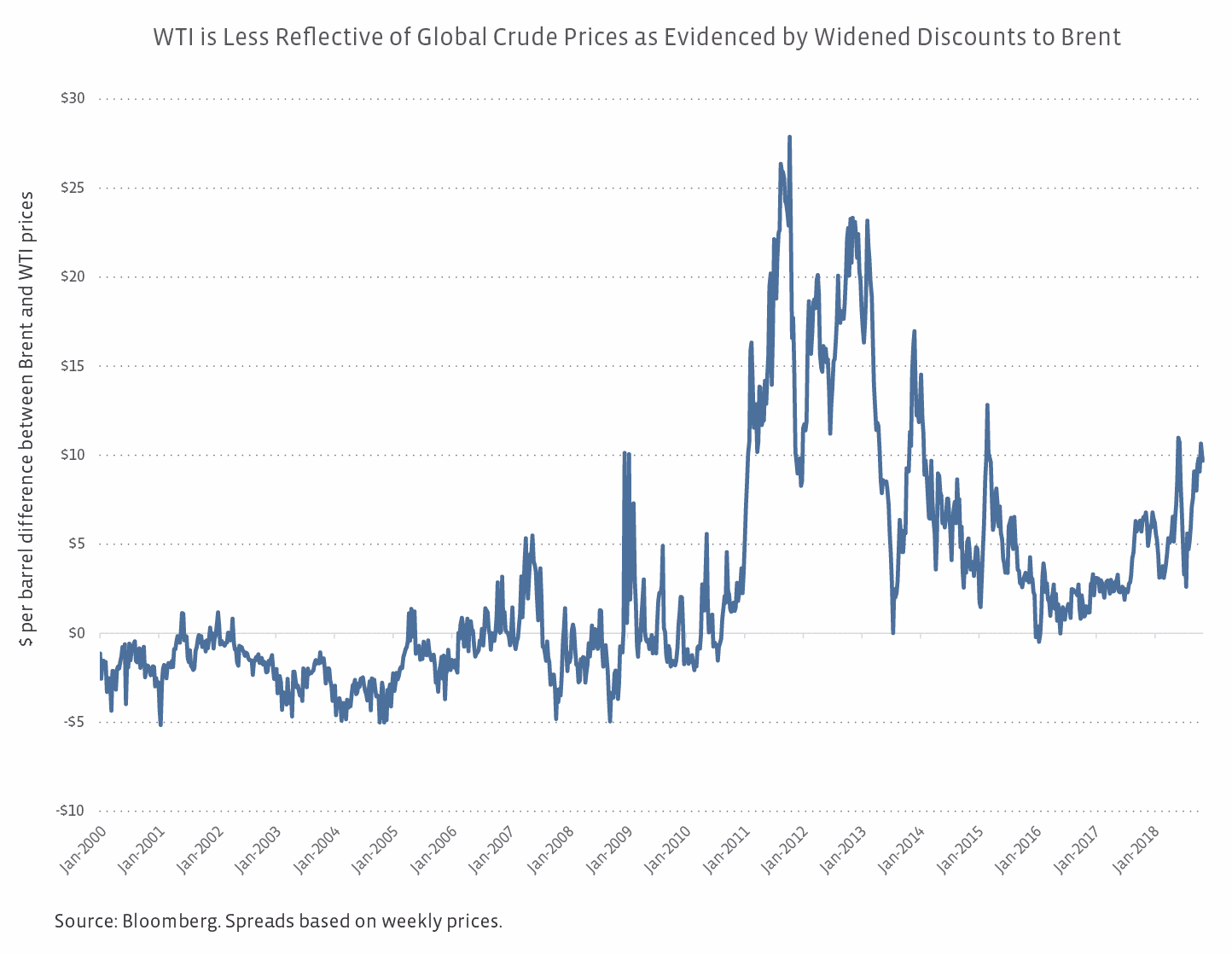

In some ways, Cushing is more of a through point than an end destination. That said, the sheer amount of infrastructure at Cushing and the number of pipelines connecting through Cushing merit the continued tagline of “pipeline crossroads of the world.” Cushing has over 75 MMBbls of working storage capacity, over 3.5 MMBpd of inbound pipeline capacity, and approximately 3 MMBpd of outbound capacity. Its central location adds to its importance as a physical hub, even though its landlocked position renders the WTI contract less useful for exports as discussed.

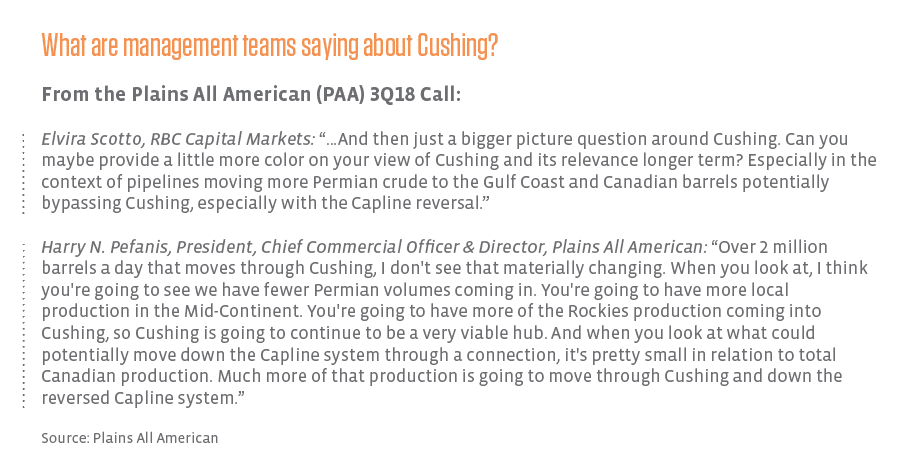

If Cushing was losing relevancy as an oil hub, you would not hear about potential newbuild pipelines originating in Cushing, expansions of pipelines out of Cushing, and storage additions. Phillips 66 (PSX) announced an open season last week for the Red Oak Pipeline from Cushing to Texas destinations, including Houston, Corpus Christi, and Beaumont. In addition, Tallgrass (TGE) recently proposed the Seahorse Pipeline from Cushing to St. James, and Magellan Midstream Partners (MMP) and Navigator Energy Services have launched an open season for the new Voyager Pipeline from Cushing to Houston. There have also been recent expansions of existing pipelines in and out of Cushing, including MPLX’s (MPLX) expansion of the Ozark Pipeline from 230 to 345 MBpd this year and Navigator Energy Services’ expansion of the Glass Mountain Pipeline. Plains All American (PAA) is also considering expansions of its Red River and Diamond Pipelines from Cushing, with Diamond to potentially extend to Capline. Keyera (KEY) is developing a new crude storage and blending terminal at Cushing.

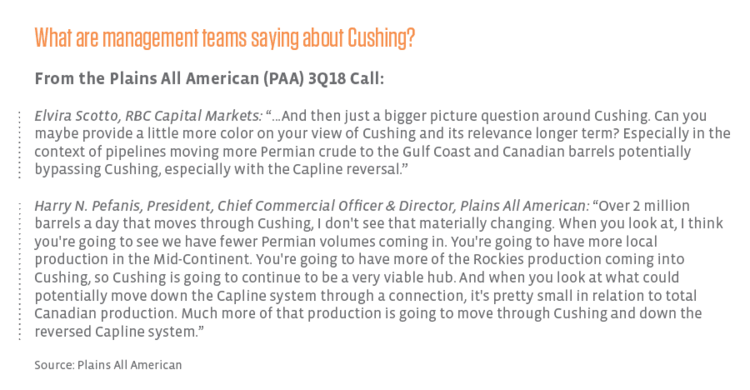

One could argue that production growth in Texas has made Cushing less relevant. With the exception of volumes shipped on the 450-Mbpd Basin Pipeline from the Permian to Cushing, Permian and all Eagle Ford oil production bypasses Cushing and ships directly to the Gulf Coast. Even Bakken production can bypass Cushing with Energy Transfer’s (ET) Bakken Pipeline System running from North Dakota to Texas via the oil hub in Patoka, Illinois. Nonetheless, Cushing is a key destination for production from the Rockies (Colorado and Wyoming) and Canada, as discussed in the quote below.

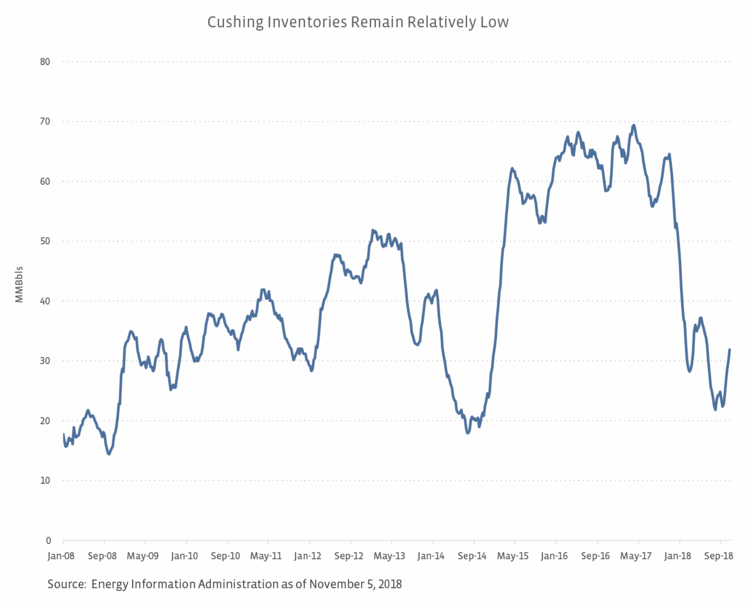

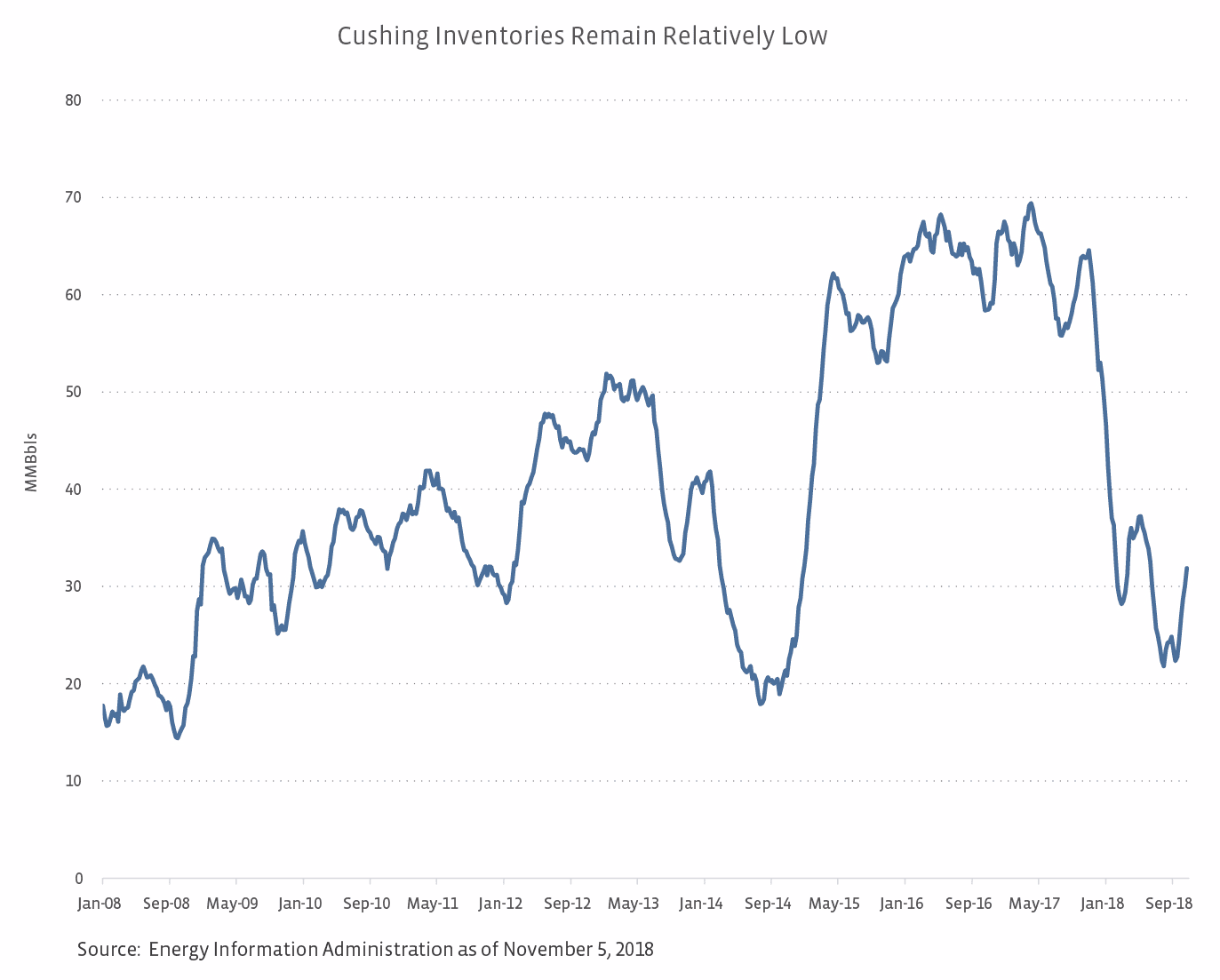

Additionally, it’s easier to question Cushing’s relevance as an oil hub when inventories are relatively low, as shown below. Inventories have started to rebound with refinery maintenance season (lowers oil demand) and contango at the front of the forward curve (read more). If the WTI futures curve was in contango across the curve and Cushing inventories were at levels pushing towards 70 MMBbls, there would probably be less talk of Cushing being irrelevant.

For its part, Houston is an end destination and a launching point for crude exports, with access to Permian barrels and even Canadian barrels via Cushing. Outside of Houston, there are several notable crude terminals and hubs on the Gulf Coast – Nederland, Freeport, Corpus Christi, and Port Arthur in Texas, and St. James in Louisiana. There are no real alternatives near Cushing. The alternatives available on the Gulf Coast could potentially cap Houston’s prominence, but the amount of nearby infrastructure (and potential connectivity with that infrastructure) appears a positive, with MMP contemplating a new crude pipeline from Houston to Corpus Christi.

Bottom line

Cushing and Houston are both important oil hubs, with Cushing representing the established hub and Houston proving more of an up-and-comer by comparison. Houston’s rise to prominence in recent years has been largely driven by direct connections to the Permian and the growing crude export opportunity. Despite Cushing’s maturity, there are still growth opportunities for new pipelines connected to the hub, including two proposed pipelines from Cushing to Houston. While we’re hesitant to say Houston is the new Cushing, we do think both provide important functions as physical hubs, and both WTI and Houston futures contracts serve to meet the specific needs of market participants.

{kind=link}

{kind=link}

{kind=link}