This basin measures 250 miles wide by 300 miles long and gets its name from the Permian geological period.

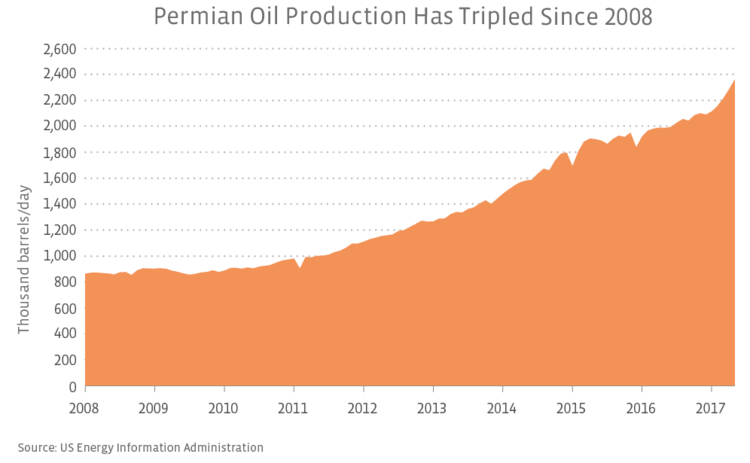

Everyone is talking about the Permian because oil production there has TRIPLED since 2008.

Even during the recent energy downturn, the Permian kept pumping, increasing production in all but three months between January 2016 and March 2017. The US Energy Information Administration (EIA) recently released a report detailing that 340 of the 857 total rigs in the US are in the Permian. That’s 40%, y’all!

The Permian has been a steady production area for about a century. Many years ago, however, the oil was perceived to be drying up and big oil companies sold their positions in the basins to smaller producers. The idea was that the little guys could scrape out the last of the oil as the Permian declined. But things changed rapidly with the invention of hydraulic fracturing. With new technologies in play, oil started to flow out of the Permian again. Exxon Mobil (XOM) bought 275,000 acres in the Permian in mid-January of this year to double its holding, and they aren’t the only oil giant re-focusing on the area. Chevron (CVX) boasts its ownership of roughly 2 million acres in the region and notes its production of around 90,000 barrels of crude oil each day.

Thanks to the geological layering of the area and the fact that lots of infrastructure is already built out in the Permian, break-even costs are lower than in many other basins. In the fourth quarter of last year, some speculated that the break-even cost in the Delaware Basin (a subsection of the Permian) was as low as $37 per barrel.

Given all of this, it only stands to reason that this is an area of extreme interest for MLPs. There has been lots of debate over if there is a need for more takeaway capacity out of the Permian. Some analysts think the region could be in danger of becoming over built because of all the new project announcements. However, with three times more production than we saw in 2008 and the expectation that it may continue to climb, many MLPs and energy infrastructure companies are getting a piece of the action. For example, Plains All American Pipeline (PAA) announced an open season for an additional 350,000 bpd of crude oil pipeline capacity from the Permian to Cushing on April 18. This is in addition to its JV with Noble Midstream Partners (NBLX) to acquire the Advantage Pipeline in the Delaware Basin, its agreement to acquire a Permian Basin crude oil gathering system, another JV with Magellan Midstream Partners (MMP) to expand the BrideTex Pipeline’s capacity, and its expansion of the Cactus pipeline. Buckeye Partners (BPL) is also part of the so-called “Permania” given its announcement for an open season on a crude oil pipeline running from the Permian to Corpus Christi. Notably, MMP is considering construction of a crude oil and condensate pipeline along the same route.

We also know that where there is crude, there is natural gas. Kinder Morgan (KMI) and DCP Midstream (DCP) proposed a new project to take natural gas out of the Permian. The Gulf Coast Express Pipeline Project would carry 1.7 million Dth/d out of the basin running from Waha, Texas to Agua Dulce, Texas. Further, Targa Resources Corp (TRGP) announced last week that it would be building two additional natural gas processing plants in the Midland and Delaware Basins representing an additional 450 MMcf/d of capacity. Energy Transfer Partners (ETP) also announced plans for a 200 MMcf/d processing plant during its May 4th earnings call.

With low break-even costs and production flowing, it’s no wonder everyone is talking about the Permian. In the days ahead, we’ll be keeping tabs on the various open seasons. If all these projects get commitments, the Permian Party could be the event of the year!