My son has a little plastic “fun bus” that is his most prized possession. The fun bus has been thrown off the side of the banister, pushed down multiple slides, sat on, run through the conveyor belt at the airport, and toted around by my toddler wherever he goes. Every time I see the fun bus fly in the air, I steel myself for it to fall apart. But, that thing was made to last. In a similar way that the fun bus takes a lickin’ and keeps on tickin’, so it goes with MLPs. It’s no secret that MLPs had a rocky ride during the recent energy cycle. We’ve seen lots of consolidations in the past few months and many MLP investors are wondering if the MLP model is bound to fall apart. None of us know the future, but for now, I think it’s fair to say that the fun bus and MLPs are two vehicles that will keep rolling.

Private Letter Rulings (PLRs) Indicate New MLPs on the Horizon

MLPs hit their low on February 11, 2016. Since that time, there have been twelve affirmative private letter rulings released. Just to refresh your memory, companies that are unsure if a particular business activity is considered qualifying under Section 7704 of the US Code will write to the IRS and ask for a formal opinion. The company seeks to receive written confirmation from the IRS (in the form of a PLR) concluding that certain operations qualify to be structured as an MLP. There are times where a company that is already an MLP will consider adding a business activity to its existing operations and will seek a PLR. However, PLRs are typically requested from businesses planning to create a new MLP. Given the number of PLRs that are still being released from the IRS (despite the updated qualifying income regulations that were intended to result in fewer PLRs), it’s fair to say that many “energy parents” are considering an “MLP baby.”

PLRs are largely redacted, but if you’d like to read the details of those listed in the timeline, you can find them in the IRS database by clicking here. It’s worth noting that many of the PLRs address more non-traditional activities such as fluid handling and disposal services for oil and gas producers.

Companies Are Still Forming and Considering the MLP Structure

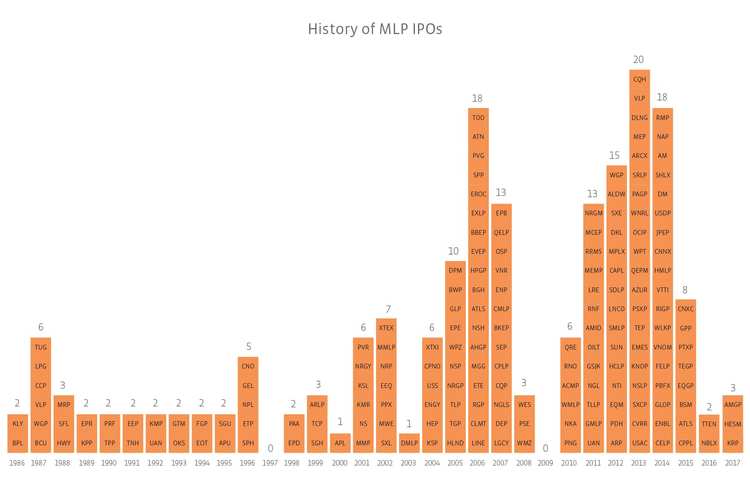

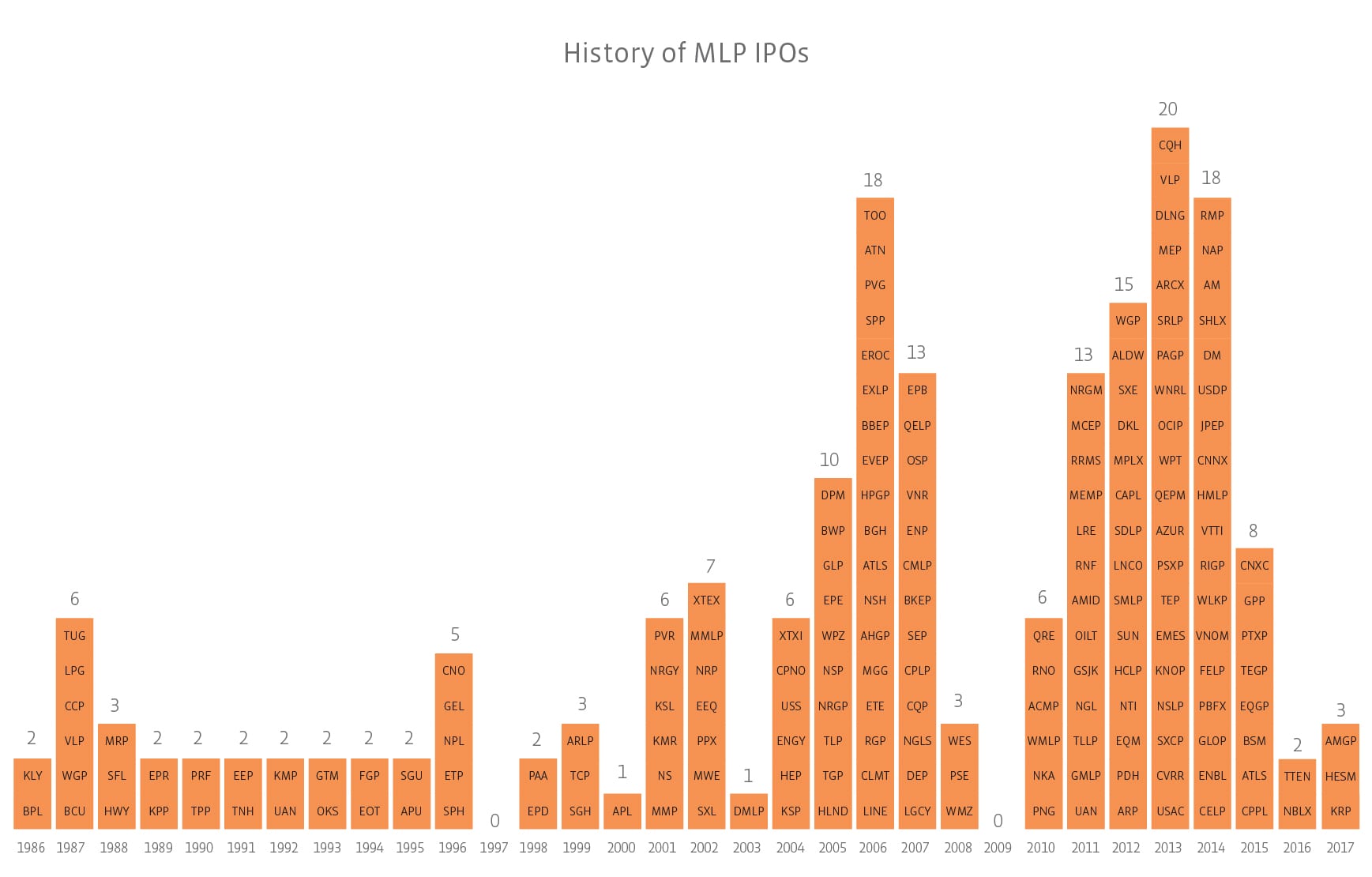

We’ve seen three IPOs this year. No, it’s not the boom we saw in 2013 and 2014, but we’re already ahead of last year. The MLPs born in 2017 are:

Kimbell Royalty Partners (KRP) on 2/2/17

Hess Midstream Partners (HESM) on 4/4/17

Antero Midstream GP (AMGP) on 5/4/17

KRP is the smallest of the three with a market cap of only $262 million as of Alerian’s June rebalancing. HESM is substantially larger with a market cap of $1.2 billion and AMGP is the biggest of the three with a market cap of $3.9 billion.

Along with the companies seeking PLRs, there is at least one very familiar name that is considering an MLP. Last week, BP (BP) announced that it might pursue an IPO of its midstream assets by forming BP Midstream Partners. There has also been chatter of energy giant Chevron (CVX) creating an MLP to produce more value on its position in the Permian, but no formal comments from the company.

In short, Alerian believes there is lots of life left in the MLP model. In her next post, Alerian’s Director of Research will take a closer look at the future of MLPs by exploring the consolidations we’ve seen, explaining whether we’re at the end of the consolidation cycle, and discussing what’s next for the MLP space.

{kind=link}

{kind=link}