US midstream expanding its horizons overseas.

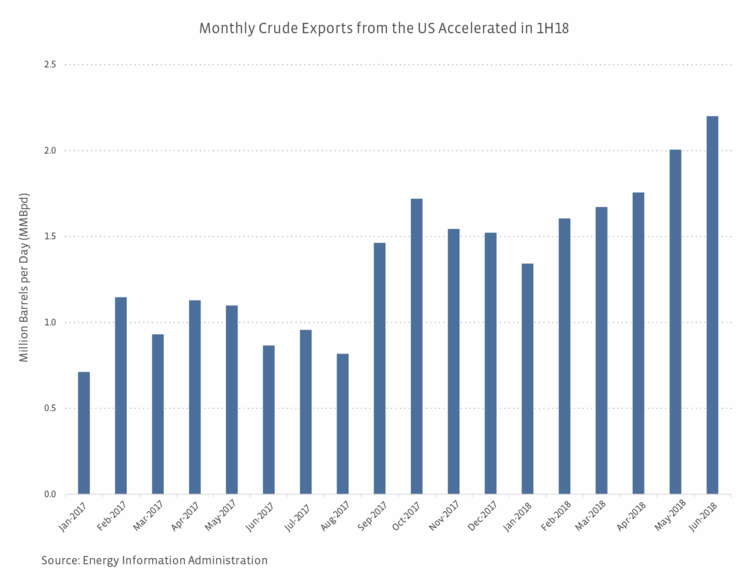

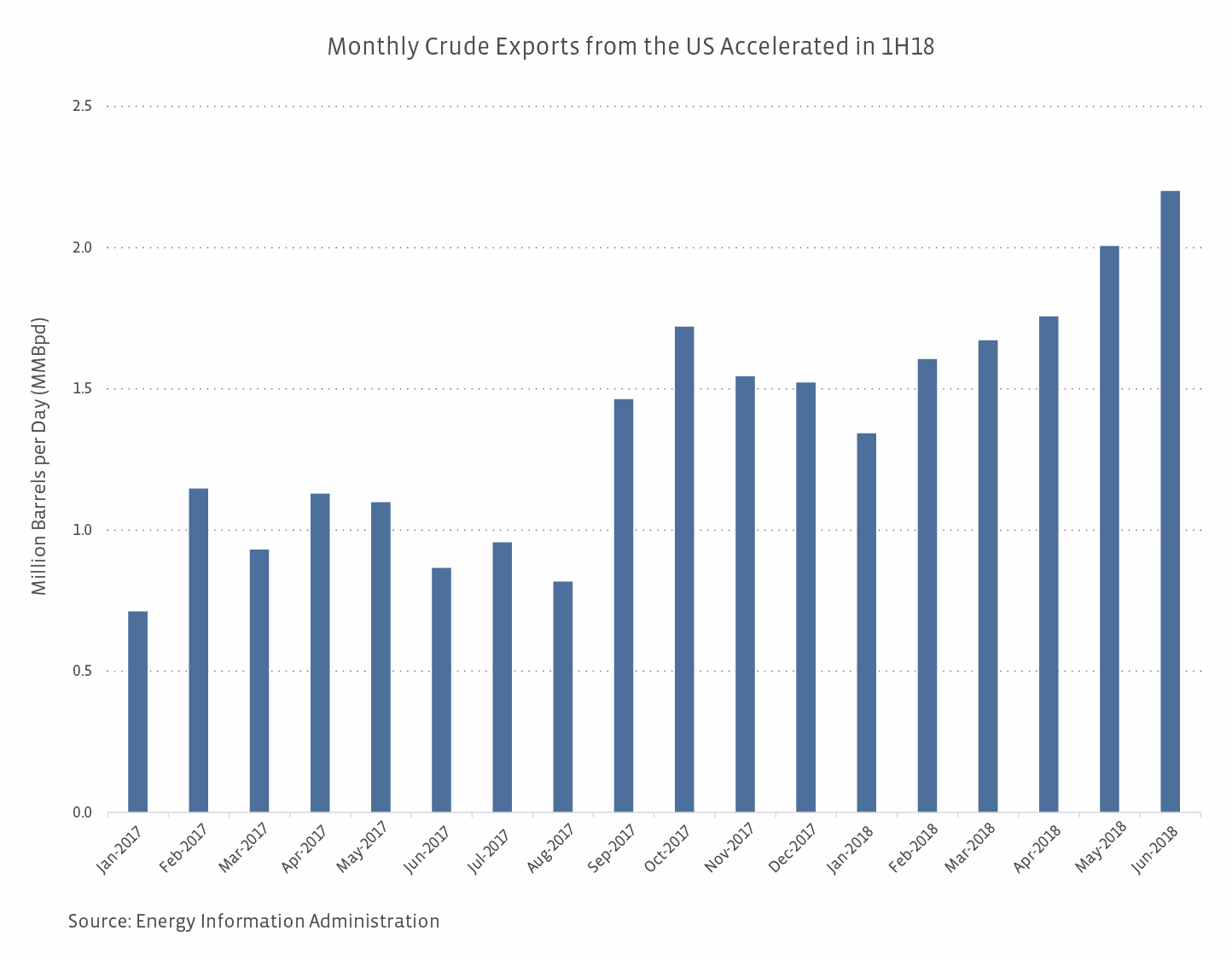

In May 2018, monthly US exports of crude oil exceeded 2.0 million barrels per day (MMBpd) for the first time ever and were double the volumes exported a year earlier in May 2017. Framed another way, the US exported nearly 20% of its daily oil production of 10.4 MMBpd in May. Looking at the most recent monthly data, June exports of 2.2 MMBpd represented 20.6% of US crude production for the month. With US oil production expected to grow by 1.3 MMBpd in 2018 and 1.0 MMBpd in 2019, crude exports will continue to grow as well. Even the Louisiana Offshore Oil Port (LOOP), which is the largest entry point for bringing waterborne crude into the US, has begun exporting crude. LOOP can load the aptly named Very Large Crude Carriers (VLCC), which carry ~2 million barrels (MMBbls) of crude.

We’ve seen several project announcements from midstream companies this year focused on crude exports:

Tallgrass Energy (TGE) announced plans for a new crude pipeline from Cushing, Oklahoma, to St. James, Louisiana, and a separate liquids terminal that will be able to load and unload Post Panamax vessels and barges. TGE expects to build an offshore pipeline to allow for loading VLCC as well.

Enterprise Products Partners (EPD) plans to develop a crude export terminal off the coast of Texas, which will be capable of loading VLCC.

Magellan Midstream Partners (MMP) and LBC Tank Terminals plan to add storage capacity and a new Suezmax dock to expand their Seabrook Logistics joint venture.

Buckeye Partners (BPL), Phillips 66 Partners (PSXP), and Andeavor (ANDV) plan to build a crude export terminal in Ingleside, Texas, with two docks capable of accommodating VLCC.

That may seem like a lot of projects or maybe even a potential overbuild when considering the US exported 3.0 MMBpd of crude at its peak this summer based on weekly export data. However, it’s important to keep in mind that loading ships takes time. While a VLCC can carry ~60% of one day’s oil production from the Permian Basin based on recent production of 3.4 MMBpd, it may take a week or ten days to load 2 MMBbls of crude onto the tanker. If it takes ten days to load, that VLCC accounts for less than 6% of Permian production for the ten-day period. Of course, smaller ships will take less time to load, but loading a ship is not instantaneous. With that context, it’s easy to see how more export infrastructure will be needed to keep up with growing production.

IMO 2020 may further support export growth.

While IMO may stand for “in my opinion” according to linguistic authority Urban Dictionary, energy observers know IMO as the International Maritime Organization. In 2016, the IMO announced that the sulfur content in marine fuels would have to be reduced from 3.5% to no more than 0.5% by the start of 2020. The rule has far-reaching implications for the shipping and refining industries, but we’ll focus on the implications for US crude exports.

In short, the IMO requirement is likely to result in increased global demand for sweet crudes (sulfur content less than 0.3%), particularly from less complex refineries overseas that are not well configured to remove sulfur from crude. As detailed in this piece from the Energy Information Administration, oil production growth in the US has been mostly in light, sweet crude. Thanks to the IMO regulations, light, sweet crude may be in higher demand come 2020, providing further support to US crude exports. For reference, the weighted average sulfur content of crudes processed by US refineries was 1.38% in June 2018, and the vast majority of distillate production from US refineries has a sulfur content of 15 parts per million or less (i.e. ultra-low sulfur diesel). Given their complexity, US refiners will not need more light, sweet crude to produce low-sulfur fuel, but less complex refineries overseas likely will.

Should crude exporters be worried about trade wars?

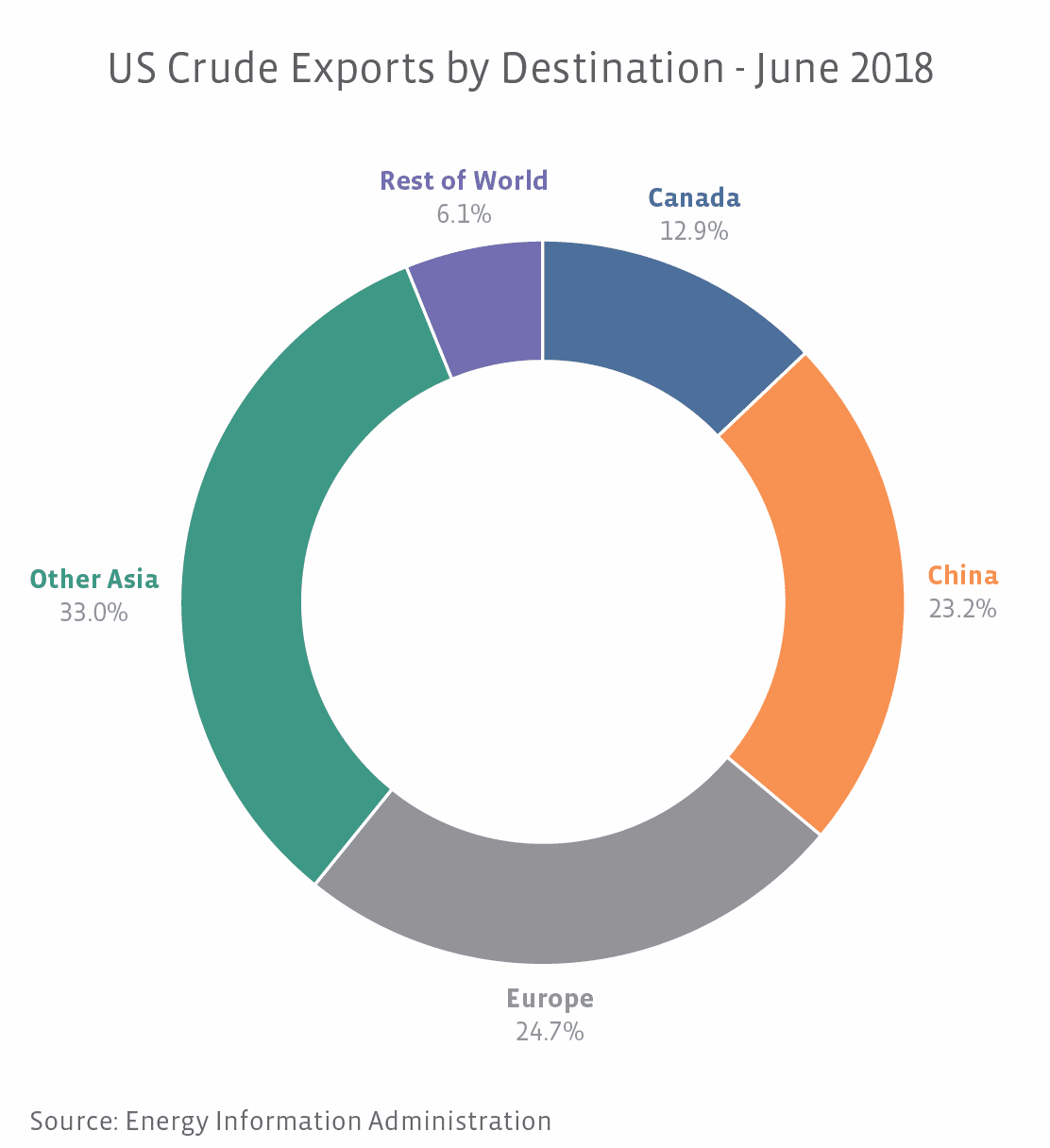

While the US exported crude to 37 different countries last year, its biggest customers were Canada and China, accounting for 30.5% and 19.1% of US crude exports. US trade relations with both countries have been making headlines recently. Last month, China removed crude from a list of tariffs on US exports, but policy uncertainty is reportedly impacting export volumes despite crude not being on the list. Meanwhile, Canada’s inclusion in a new trade agreement between the US and Mexico remains in limbo.

Canadian crude imports into the US vastly overwhelm US crude exports to Canada. In 2017, Canada exported nearly 4 MMBpd to the US, while the US exported 354,000 bpd to Canada, over an 11x difference. Energy does not seem to be in the crosshairs, but negotiations are ongoing. US refineries need Canadian heavy crudes, and Canada needs access to US demand. Any deal that would infringe on crude trade between the US and Canada would likely be a lose-lose for both countries.

Similarly, when it comes to oil trade, the US is a desirable supplier for China, and China is a desirable customer for the US. The pace of China’s oil demand growth has moderated, but net imports are still forecast to grow by about 25% from ~8 MMBpd today to ~10 MMBpd by 2023, according to the IEA. With the US expected to drive more than half of global oil supply growth and China already importing significant volumes of US crude, it may be more difficult to satisfy increased demand without US oil. For the US, the demand growth expected in China makes it an attractive customer. As shown below, US crude exports had several end destinations in June, but China accounted for nearly a quarter of US crude exports. It also bears mentioning that US crude exports to China were at a record high in June 2018 of 0.5 MMBpd. If US crude exports to China are subject to tariffs and Chinese demand for US crude diminishes, US exporters will look to satisfy demand in other markets, just as China would look to replace US supply.

Bottom line

Crude exports are poised for growth as the US progresses toward becoming the world’s top oil producer. To prepare, midstream companies are building and expanding crude export terminals to satisfy demand from overseas as crude exports provide another avenue for growth. IMO 2020 may further incentivize exports of light, sweet crude from the US. While trade relations remain dynamic, it seems unlikely that US crude exports will be derailed by trade policy given the importance of US oil supply to meeting growing global energy demand.

{kind=link}

{kind=link}