To help investors keep up with the markets, we present our ETF Scorecard. The Scorecard takes a step back and looks at how various asset classes across the globe are performing. The weekly performance is from last Friday’s open to this week’s Thursday close.

- British Prime Minister Theresa May reached out to U.K.’s Labour Party in a bid to push a deal through Parliament before the country is expected to exit the European Union on April 12. The Parliament marginally passed a bill on Wednesday to block a no-deal Brexit, likely paving the way for a delay of the actual date and a softer Brexit. Both the Labour opposition and May said they had constructive discussions and planned to meet again. May also officially requested the EU to postpone the exit day until June 30.

- Chinese manufacturing purchasing managers’ index (PMI) crawled into expansion territory to 50.5 in March, beating expectations of 49.6. Caixin’s manufacturing PMI, released a day after the official figure on Saturday, jumped to 50.8 from 49.9

- A host of European manufacturing PMIs came in worse than expected and most of them were in contraction territory. French, German and Italian PMIs were all below 50, with only Spain’s PMI moving into expansion area at 50.9. Europe-wide manufacturing PMI stood at 47.1, the second consecutive month of contraction. Such a low level has not been seen since April 2013.

- Meanwhile, European services PMIs were largely in positive territory. Germany, Italy and Spain were all in growth mode, while the Spanish index was in slight contraction. Overall, Europe’s final services PMI came in at 53.3, beating expectations of 52.7.

- European inflation fell back to 1.4% in March year-over-year, while the core consumer price index (CPI), which excludes volatile food and energy prices, declined to 0.8% from 1% previously.

- U.S. retail sales fell 0.2% in March compared to the previous month, while core retail sales declined by 0.4%. Analysts had expected retail sales to rise 0.3%.

- U.S. manufacturing PMI is largely unchanged at 55.3, which indicates expansion. Still, this is the lowest reading since June 2017.

- U.S. durable goods orders declined 1.6% in February, versus expectations of a 1.1% fall. Core durable goods orders, which excludes large orders such as aircraft, rose 0.1%, lower than analysts’ forecasts of 0.3%.

- ADP said the U.S. economy added 129,000 jobs in March, down from 197,000 in the prior month and below forecasts of 184,000. The more important government report is scheduled to be released on Friday.

For more ETF news and analysis, subscribe to our free newsletter.

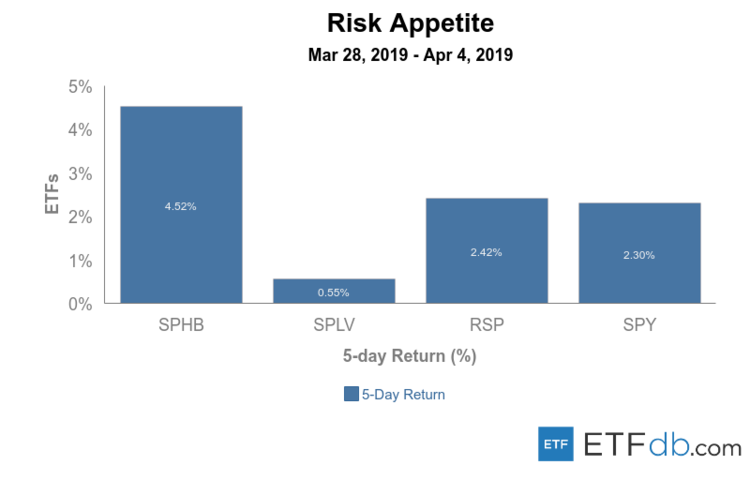

Risk Appetite Review

- Risk assets (SPHB ) were the best performers this week, rising 4.52%, amid a rebound across the board.

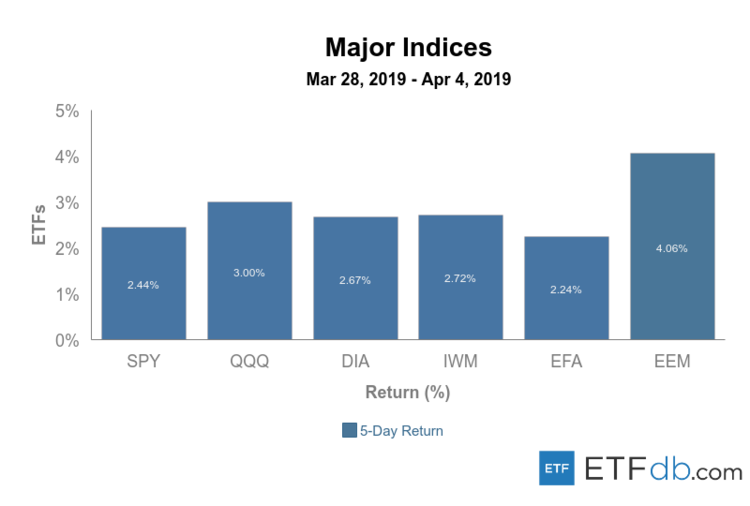

Major Index Review

- Major indexes rebounded this week.

- Emerging markets (EEM ) surged more than 4% this week, by far the best performer from the pack.

- (EFA ), the index composed of developed market equities excluding U.S. and Canada, posted the smallest gains for the week, rising 2.24%.

To see how these indices performed over the past year, check out ETF Scorecard: March 29 Edition

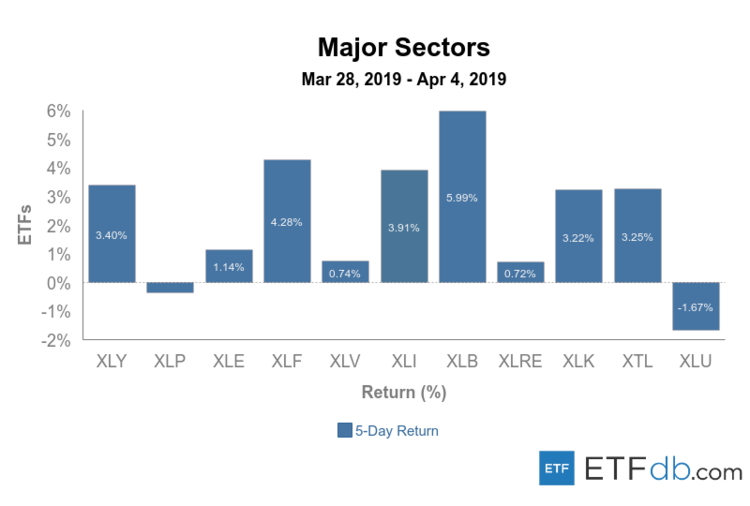

Sectors Review

- All sectors were up with the exception of energy and utilities.

- Materials (XLB ) advanced nearly 6%% for the week, representing the best performance from the pack.

- At the other end of the spectrum were utilities (XLU ), which were down 1.67%.

Use our head to head comparison tool to compare two ETFs such as (XLB ) and (XLU ) on a variety of criteria such as performance, AUM, trading volume and expenses.

Foreign Equity Review

- Foreign equities were all up.

- Highly volatile Brazil equities (EWZ ) surged 7.29%, rebounding after a fall due to worries a plan to reform the country’s pension system will fail. To soothe lawmakers, the government did not rule out making concessions.

- Russian equities (RSX ) were the worst performers for the week, declining around 1%.

To find out more about ETFs exposed to particular countries, check our ETF Country Exposure Tool. Select a particular country from a world map and get a list of all ETFs tracking your pick.

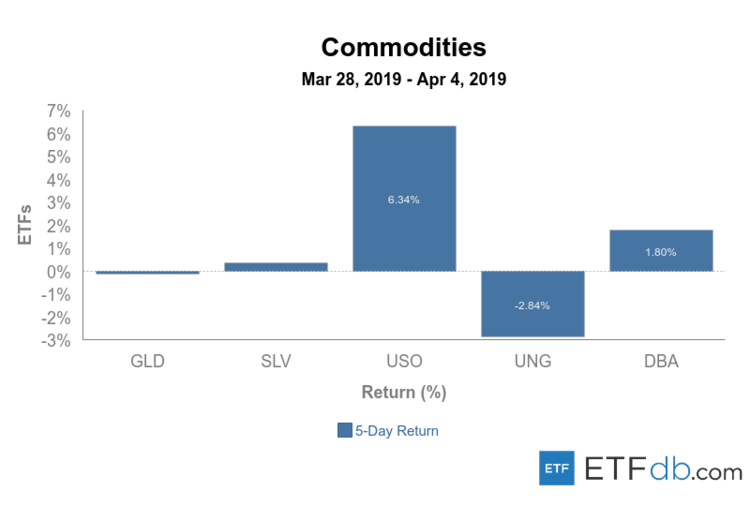

Commodities Review

- Despite a colder-than-usual winter, natural gas prices (UNG ) continued to plunge this week, down by 2.84%.

- Meanwhile, crude oil (USO ) is on an upswing, rising 6.34% this week and becoming the best performer for two consecutive weeks.

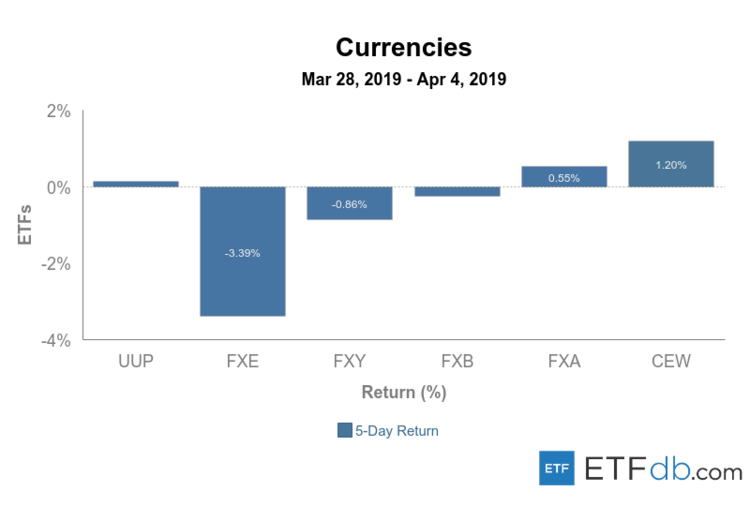

Currency Review

- Euro (FXE ) is again the biggest loser this week, down 3.39%, as a string of sentiment indexes indicated a deceleration of economic growth.

- Emerging market currencies (CEW ) gained 1.2% this week, the best performance from the pack.

For more ETF analysis, make sure to sign up for our free ETF newsletter.

Disclosure: No positions at time of writing.