What is OPEC and why should MLP investors care?

The Organization of the Petroleum Exporting Countries (OPEC) is an intergovernmental organization that coordinates oil policies among member countries. Regularly referred to as the “oil cartel,” this group has the power to regulate a significant portion of the world’s oil supply and therefore has a huge hand in the supply side of the oil price equation. The stated mission of the group is to “ensure the stabilization of oil markets in order to secure an efficient, economic and regular supply of petroleum to consumers, a steady income to producers and a fair return on capital for those investing in the petroleum industry.”

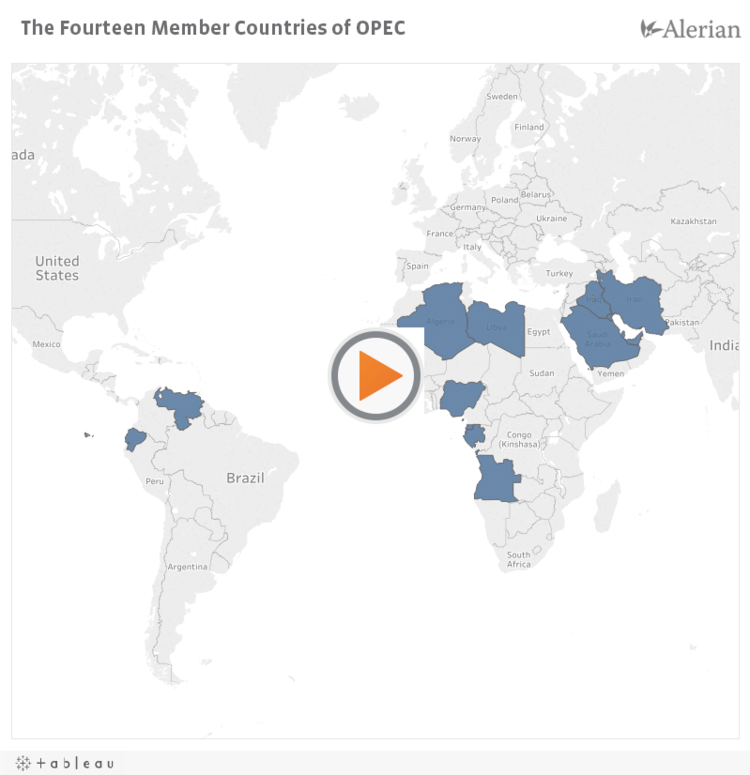

There are currently 14 member countries:

- Iran

- Iraq

- Kuwait

- Saudi Arabia

- Venezuela

- Qatar

- Libya

- United Arab Emirates

- Algeria

- Nigeria

- Ecuador

- Gabon

- Angola

- Equatorial Guinea

These countries together account for nearly 40% of global oil production and about 60% of the petroleum traded around the world. Therefore, when the group meets, the world watches. OPEC typically convenes twice a year in Vienna, Austria, where it is headquartered, but will hold additional sessions when needed. This year, OPEC met on May 25th and November 30th.

The production cuts in effect today were initially put in place at the November 30, 2016 meeting where members agreed to decrease output by 1.2 million barrels a day. Concurrently, non-OPEC producers agreed to cut production by 558,000 barrels per day, with more than half of the cut coming from Russia. At the May 25, 2017 meeting, OPEC agreed to extend production cuts through March 2018. At the recent meeting on November 30, the cuts from OPEC and non-OPEC countries were extended through the end of 2018. According to OPEC’s press release following the conference, the goal in reducing output through 2018 is to continue the group’s vision of having a “stable and balanced oil market.”

The decisions of OPEC are important to MLP investors because what the organization chooses to do affects the global oil market. In November 2014, OPEC left production quotas unchanged despite falling oil prices, choosing to defend its market share instead of the oil price. The combination of new drilling technologies in the U.S. and high OPEC production from 2014 to 2016 contributed to the oil glut of the last few years. In February of 2016, oil was around $30 per barrel and, although we like to think MLPs are oil price agnostic, that’s not necessarily the case. At a certain point, it isn’t profitable for producers to drill new oil wells, and additional midstream activities aren’t needed as much. We saw the AMZ hit a bottom in February 2016, which is also when oil prices bottomed. WTI oil prices have recovered to the mid to high $50s per barrel as of early December 2017 in large part due to the production cuts from OPEC and non-OPEC producers.

Regardless of how closely midstream energy businesses track the price of crude, stable oil prices can only be a good thing for the space. All eyes will be on the “oil cartel” when they meet again on June 22, 2018 and evaluate the oil market rebalancing. Will the cuts remain in place at current levels through the end of 2018 as currently planned? Or will OPEC begin to implement an exit strategy and potentially start to raise production? We’ll have to wait and see.