For many years, the 529 plan was a straightforward investment vehicle. Parents saved for college, children used the funds for tuition, and penalties were incurred for any remaining funds. However, the 529 and its cousin, the ABLE (529A) account, have become versatile financial tools almost halfway through 2026.

Key Takeaways:

- Total assets in education and disability savings programs reached $595 billion in the first quarter of 2026, marking a significant increase in adoption for both 529 and ABLE accounts.

- Legislative updates have introduced the grandparent loophole and doubled the K-12 withdrawal limit to $20,000, allowing families to use these plans more effectively for private education and financial aid planning.

- The ability to roll over up to $35,000 of unused funds into a Roth IRA has transformed the 529 plan from a strict college fund into a versatile retirement starter kit that eliminates overfunding risks.

See more: 529 Plan Tax Deductions for Every State

Surge in Adoption

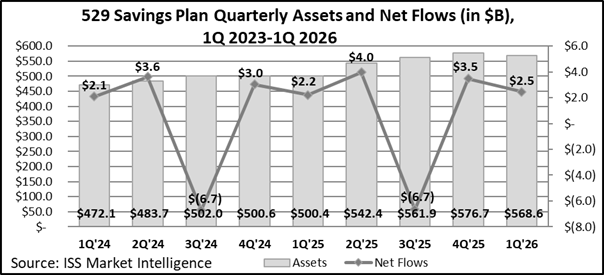

The growing popularity of these 529 plans is evident in the assets they’ve amassed. According to data from ISS Market Intelligence, the total assets under management (AUM) for education and disability savings programs hit $595 billion in the first quarter across 17.9 million accounts.

To punctuate this Q1 data further, net inflows for 529 college savings plans also hit $2.5 billion, which is up from $2.2 billion from the previous year. Despite volatility in Q1, the broad market has been humming along, adding for this growth. Also, there’s been a fundamental shift in how American families view educational savings. One prime theme is the need for greater flexibility.

Of the total assets, 529 savings plans account for $569 billion invested across 17.1 million accounts. This is a sizeable bump up from the $500 billion held in 16.3 million accounts just last year. Additionally, ABLE accounts — which offer tax-advantaged savings for individuals with disabilities — have also witnessed greater adoption. These accounts grew to 246,000 holding nearly $3.3 billion in assets, which is also higher than the $2.5 billion recorded last year.

ISS Market Intelligence also revealed the top 529 program managers and plans in Q1:

The 529 market remains highly concentrated among a few elite program managers and plans. As of Q1 2026, the five largest program managers include:

| Program Manager | Q1 2026 Assets ($B) |

|---|---|

| Ascensus | $155.20 |

| American Funds | $104.90 |

| TIAA | $83.50 |

| Fidelity | $56.30 |

| State of Utah | $29.20 |

In terms of AUM, the CollegeAmerica 529 Savings plan by American Funds sits atop the provider leaderboard.

| 529 Savings Plan | Provider | Q1 2026 Assets ($B) |

|---|---|---|

| CollegeAmerica 529 Savings | American Funds | $104.90 |

| New York 529 Direct | Vanguard | $50.40 |

| Vanguard 529 | Vanguard | $43.30 |

| My529 | Utah | $29.20 |

| UNIQUE College Investing Plan | Fidelity | $28.10 |

Expansion & "Grandparent Loophole"

As mentioned, flexibility is top-of-mind with American families when it comes to college education savings. That said, the 529 plan’s utility for younger students is evolving.

The annual withdrawal limit for qualified K-12 expenses doubled in size, moving up from $10,000 to $20,000 per student at the start of 2026. This reflects the changing landscape of American education, where private schooling, specialized tutoring, and educational therapies are becoming more common amongst families.

Another hot button topic for 529 plans is how they affect college financial aid. Under the Simplified FAFSA rules debuting in the 2024-2025 cycle, the “Grandparent Loophole” was introduced. In the past, distributions from a 529 plan owned by a grandparent counted as untaxed student income. In turn, this could reduce the amount of financial aid eligibility by as much as half of the distribution amount. According to the new rules, grandparent-owned 529 accounts are not reported on the FAFSA at all. Additionally, distributions are no longer counted as income. For families with a high net worth, this makes grandparent-owned accounts a helpful tool when it comes to obtaining assistance for college costs without harming a student’s ability to receive need-based aid.

The Roth IRA Rollover

As mentioned, the 529 plan is evolving from simply just a pay-for-college fund. It can also help kickstart a child’s retirement through a Roth IRA. Thanks to the latest superfunding rule, plan participants can move up to $95,000 (or $190,000 for couples) into the 529 plan in a single year without triggering gift taxes.

Furthermore, plan participants now have the ability to roll over unused 529 funds into a Roth IRA. As mentioned earlier, unused funds in years past came with penalties. As such, families would avoid overfunding a plan if a child received a scholarship or decided to bypass college completely. Starting in 2024 (now fully integrated into 2026), account owners can roll over up to $35,000 (lifetime limit) per beneficiary into a Roth IRA. Given this more recent provision, it effectively turns a 529 plan into a retirement starter kit, which eliminates the “use it or lose it” scenario.

Growth Up Ahead

Looking ahead, there’s more growth to be realized for 529 plans. ISS Market Intelligence is already forecasting ongoing growth over the next three to five years.

“Building on the momentum of increasing utilization, the recent expansion of qualified 529 expenses to more K-12 related expenses beyond tuition, to credential programs, and workforce-oriented training programs positions the 529 industry for continued growth,” ISS Market Intelligence said.

A confluence of legislative changes, more qualified expenses, and greater economies of scale are expected to drive this growth. By stripping away limitations from yesteryear, 529 and ABLE plans have become the flexible financial tools that families need today.

Originally Published on Advisor Perspectives

For more news, information, and strategy, visit ETFdb.